This Stock Could Make You Millions

Wall Street analysts tend to be one-dimensional, focusing on esoteric data while ignoring common sense. In the process, they often miss the market's best opportunities.

This is great news, of course, for investors like Warren Buffett and Peter Lynch, who get rich by rejecting facts and figures in favor of investing in what they know.

The best stock in today's market fits this model like a glove. While some Wall Street analysts reject it as "the world's largest co-op," it has stacked up staggering returns for its shareholders. And in my view, Wall Street's closed-minded approach to this company makes now a great time to invest in its shares.

Costco: The Wall Street pariah

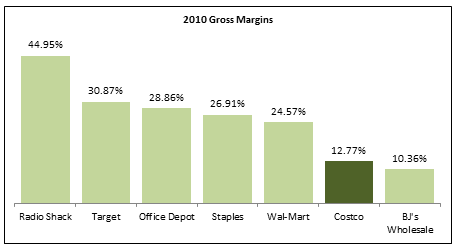

Wall Street's problem with Costco (NAS: COST) stems from its business model. According to conventional wisdom, Costco's commitment to low prices rewards customers, but hurts shareholders. Costco's gross margin, one of the most important statistics in all of retail, seems to bear this out.

As I discussed in a previous article, gross margin indicates both potential profitability and brand power. It's the portion of sales left after a company pays for all the costs directly attributable to producing (or, in the case of a retailer, obtaining) the goods it sells.

Source: Robotdough.com.

As you can see, it's hard to argue with Wall Street's logic here. Its low prices leave Costco's gross margin dwarfed by those of its close competitors Wal-Mart (NYS: WMT) and Target (NYS: TGT) . This apparent disadvantage seems even steeper when you compare Costco to more specialized retailers like Office Depot (NYS: ODP) , Radio Shack (NYS: RSH) , and Staples (NAS: SPLS) . Indeed, of the retailers I examined, Costco's gross margin only compares well against that of BJ's Wholesale Club (NYS: BJ) .

Turning of the tides

Fortunately for contrarians, Wall Street largely overlooks one key fact: The same low prices that squeeze Costco's gross margins also contribute directly to its exceptional growth. In the last five years alone, Costco grew its membership base by 25%. Much of that growth took place in the depths of the Great Recession.

Costco subsequently translated this expansion into higher same-store sales, the creme de la creme of retail statistics. Indeed, despite the recession, Costco's same-store sales increased by 5% annually -- five times the rate of Wal-Mart and Target.

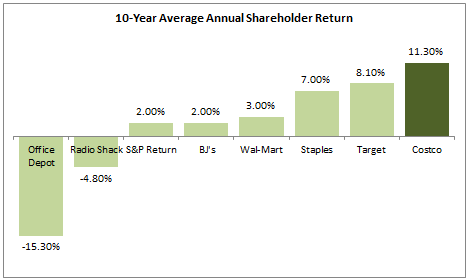

What about shareholders?

Flying in the face of Wall Street's scorn, Costco's low-margin/high-growth model has enjoyed amazing success in increasing shareholder value. As you can see, its 10-year compound annual growth rate trounces both its competitors and the market's:

Source: Yahoo! Finance.

If you'd purchased Costco shares 10 years ago, you would have almost tripled your money! That's quite a bit better than the S&P 500 index's near-flat performance over the same period.

The contrarian view

By proving Wall Street skeptics wrong, Costco reaffirmed its merit to all contrarian investors. That's why Costco is one of only two retailers our analysts recommend in their free report "The Death of Wal-Mart: The Real Cash Kings Changing the Face of Retail," which discusses how innovative retailers are actually growing revenue and making shareholders rich even in these difficult times.

At the time thisarticle was published Fool contributor John Maxfield does not hold positions in any of the companies mentioned in this article.The Motley Fool owns shares of Costco, Wal-Mart, and RadioShack.Motley Fool newsletter serviceshave recommended buying shares of Costco, Staples, and Wal-Mart, as well as creating a diagonal call position in Wal-Mart Stores. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.