Gold, Unhinged

If the question is whether gold will go higher from here, the answer is likely yes. But it may not keep rising for the reasons that gold bulls cite.

In the battle between bulls and skeptics, the bulls are clearly winning. They have the advantage of conviction; a belief that something is right is always more powerful than whether something is actually right. Those who say gold is a bubble often compare it to the dot-com boom. If they're correct, then we need to ask whether today is 1997, or 2000. It could very well be the former. But while skeptics may succumb to momentum, they shouldn't accept fuzzy arguments.

The dollar's staying put

One such argument gaining traction lately is that the price of gold isn't rising; the dollar is falling. By nearly any reasonable metric, this doesn't add up. Measured against the U.S. Dollar Index, it's false. Measured against a slew of other commodities, it's false. Measured against nominal wages, real estate, or stock prices, it's false. Measured against the Consumer Price Index -- or MIT's Billion Prices Project, if you're more skeptical -- it's false.

One metric it may stand up to is the U.S. monetary base. A Fool colleague used this argument last week to argue that gold prices "steadily tracked the amount of money in circulation over the past decade." Thus, he wrote, "an increase in the monetary base dilutes the dollar; as a result, the price of gold (and everything else) has increased. In other words, speculation has little to do with the recent rise in gold prices."

This is a rational starting point -- although "everything else" is not moving at anywhere near the pace of gold. If you want to value gold, comparing it to money circulating throughout the economy is a smart way to do so.

But the monetary base doesn't reflect the amount money circulating throughout the economy, particularly right now. Why? For the same reason that two rounds of quantitative easing did little good: The vast majority of money the Fed has "printed" over the past three years has not entered the economy. It stayed right at the Fed in the form of excess reserves. Since 2008, the monetary base has increased by $1.8 trillion, yet excess reserves held at the Fed increased by $1.6 trillion. Despite the hue and cry, the increase in money actually flowing throughout the economy -- money that can legitimately chase goods and services and push up prices -- hasn't diverged far from historic averages.

Gold vs. the actual money supply

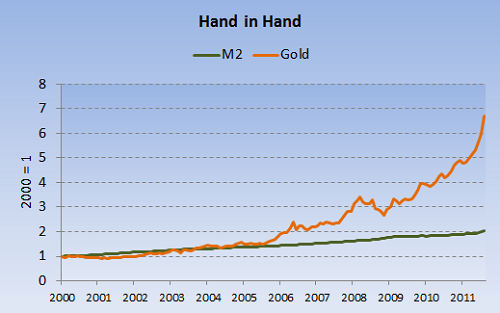

A more reasonable metric involves comparing gold to the M2 money stock. This is money that's actually in the economy, flowing through stores, sitting in people's bank accounts, and buried in backyards. Here, the story speaks for itself:

Sources: World Gold Council, Federal Reserve, author's calculations.

In numerical terms, M2 has increased 104% since 2000; gold has climbed 560%. Lest you think this is an abuse of dates, gold has increased 4,900% since the dollar's tie to the yellow metal was severed in 1971. M2 rose 1,400% over that period.

There could be an easy counter here. The monetary base may be the more relevant metric, because excess reserves can eventually snake their way into the economy, sending money supply surging. This isn't just a remote theory; it's quite likely to happen.

But when it does happen, the Fed isn't likely to sit idly by. Former Fed chairman Paul Volcker's heave of interest rates well into double-digits in the 1980s testifies to that. "The Fed is filled with serious people," said investor and commentator John Mauldin last year. "They'll try to give us inflation. Some inflation, but not hyperinflation. They know what to do with inflation. They've done this before. There's a less than 1% chance of hyperinflation."

No shiny ending to this story

There's nothing wrong with gold. There's a time and a place for it. Companies like Yamana (NYS: AUY) , Barrick Gold (NYS: ABX) , and AngloGold Ashanti (NYS: AU) will make money for their shareholders. But as Peter Tasker recently wrote in the Financial Times, "Gold generates nothing and therefore cannot be valued in its own right, only as a measure of revulsion towards other assets. Rather than being a store of value, it is doomed to obey bubble dynamics." Alas, those dynamics have created far more tears than smiles over time.

Monetary tightening isn't in the cards today or tomorrow. But when it comes, even a sniff of it, I wouldn't want to stand in its way. Many gold bulls counter that they plan on selling before that time comes. But folks, that's everyone's plan. The annoying rules of logic hold that everyone cannot get out before everyone else. The odds that gold will keep rising are good. But the odds that it will eventually end in misery are nearly assured.

At the time thisarticle was published Fool contributorMorgan Houseldoesn't own shares in any of the companies mentioned in this article. Follow him on Twitter @TMFHousel.Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.