One Medical-Device Stock I Just Bought

Welcome to my portfolio, MAKO Surgical (NAS: MAKO) . I've had my eye on you for a while, but now I'm ready to commit to a long-term relationship. I hope you stay a while.

I recently acquired a new position in the company because its robotic orthopedic surgery system, the RIO, is accelerating sales while its MAKOplasty procedures performed for minimally invasive knee surgery take off. MAKO earns revenue every step of the way. The system itself generates sales, including for installation and training, while the company sells implants and disposable products used in the procedure. It also derives some revenue from warranty and maintenance services.

Can I get your digits?

Two out of three of these revenue sources are recurring: procedures and service. Last quarter, these two recurring revenue streams accounted for 49% of revenue, compared with 44.6% a year ago. Management sees recurring revenue constituting an increasing percentage of total revenue as the company leverages its growing installed base of RIO systems.

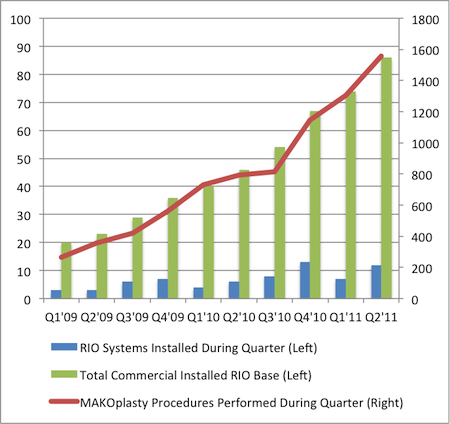

Quarterly MAKOplasty procedures performed have leapt 487% since the first quarter of 2009, going from 265 in that quarter to 1,557 in the second quarter of this year. The total commercial installed base of RIO systems has also more than quadrupled over the same time frame, from 20 to 86.

Source: 8-K press releases.

It's analogous to the razor-and-blade model, except traditionally those models make no profit on the razor and all the profit on the blades, whereas MAKO makes a healthy gross profit on its razor and even more gross profit on its blades. Last quarter, MAKO's gross margin on the RIO systems was 63.2%, and products and services boasted even higher gross margins at 77.6% and 80.8%, respectively. Each segment has expanded gross margin over the past year.

Going steady

The company hasn't been able to turn its red ink to black quite yet, and last quarter's $18.6 million in revenue -- an 81.2% increase -- resulted in a $9.9 million net loss. Selling, general, and administrative expenses are still disproportionately high since MAKO is still such a small company.

The quarter's $17.1 million in SG&A expense burned through the $13.1 million in gross profit and then some, and that's before you even include the $5 million in R&D. Still, the company has been strengthening its financial position, albeit with an equity offering last November.

Metric | 2006 | 2007 | 2008 | 2009 | 2010 |

|---|---|---|---|---|---|

Current ratio | 0.97 | 1.90 | 3.92 | 9.54 | 6.37 |

Quick ratio | 0.80 | 1.65 | 3.53 | 8.31 | 5.68 |

Source: 10-K annual reports.

MAKO is still a very small company, with a market cap of only $1.5 billion. It's competing against much larger rivals, including Stryker (NYS: SYK) and Johnson & Johnson (NYS: JNJ) , which also market orthopedic implants and knee-surgery products. The company has a long way to go if it ever wants to achieve Intuitive Surgical-esque (NAS: ISRG) success. I'm not the only one who sees similarities between Intuitive Surgical and MAKO Surgical. Foolish colleague Brian Stoffel aptly calls Intuitive Surgical an "older, more mature version of MAKO."

I tend to begin my analysis with top-line revenue growth before making my way down the income statement, and MAKO is delivering on revenue growth. MAKO is a young company experiencing all the normal growing pains of fledgling growth stocks, such as net losses. As long as MAKO can continue ramping up its installed base and MAKOplasty procedure adoption, revenue will take care of itself and net profitability and margin expansion will follow.

As of June 30 this year, there have been 8,656 MAKOplasty procedures performed. The global opportunities are just beginning. Last year, one RIO system was sold to an Italian distributor and another to a South Korean distributor for demonstration and marketing purposes to try to tap into those respective markets.

I think MAKO Surgical has the potential to be a multibagger. I must give credit to our outstanding Rule Breakers team for finding this one before I took a deeper look. They sure know how to pick 'em. Try any of our newsletter services free for 30 days, what do you have to lose? At very least, add this stock to your Watchlist.

Add MAKO Surgical to My Watchlist.

Add Intuitive Surgical to My Watchlist.

Add Johnson & Johnson to My Watchlist.

Add Stryker to My Watchlist.

At the time thisarticle was published Fool contributorEvan Niurecently purchased shares of MAKO Surgical, but he holds no other position in any company mentioned. Check out hisholdings and a short bio. The Motley Fool owns shares of Johnson & Johnson.Motley Fool newsletter serviceshave recommended buying shares of Johnson & Johnson, Intuitive Surgical, MAKO Surgical, and Stryker and creating a diagonal call position in Johnson & Johnson. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.