4 Stocks and 1 Critical Rule for a Comfortable Retirement

I'm going to give you four stock ideas I believe can help you nail down market-beating investment returns on the way to retirement. But first, there's something very, very important that we need to discuss.

Over the long weekend, I spent some time with a good friend of mine, Scott Holsopple, the CEO of the online 401(k) investment advisor Smart401k. Between college football games and burger-and-dog feeding frenzies, Scott got serious for a moment and gave me a good reminder: "Picking investments gets most of the attention from investors, but it's choosing a contribution amount that should get the focus."

Boring! Right? I'm a stock picker. I love uncovering great stocks, reading SEC filings, running valuation models, and managing my portfolio. Of course it's this kind of reaction that makes many investors ignore the contribution issue.

Scott continued: "It's easier for someone to pick a stock and think that the investment will do all of the work for them, than it is to make the decision to set aside 10% to 15% of their salary and possibly forgo a new big-screen TV."

A tale of two investors

Two investors are planning to retire 30 years from now. Both have a current portfolio of $20,000, and both want to retire with $1.25 million. One investor fancies himself a savvy stock picker and believes he can consistently earn returns of 14% per year. Picking investments is his main focus, and making a monthly $50 contribution is an afterthought.

The second investor makes saving the primary focus and she diligently puts away 15% of her paycheck, or $813 every month. She assumes that a relatively conservative mix of stocks and bonds will bring in an average of 8%, and she doesn't lose sleep over trying to earn world-beating returns.

Who crosses the finish line with a $1.25 million portfolio? They both do, more or less, finishing nearly neck-and-neck. Our saver has slightly more with a $1.3 million portfolio, while our investor has just slightly less with $1.23 million, but they're both basically right there.

But here's the problem. Choosing a monthly contribution amount is simple and within our control. If we're like the saver and choose to put 15% of our income into savings every month, then guess what? Fifteen percent of our income ends up in savings. Bam! Done. Moving on.

Investing returns are a bit more fickle. We can look at long-term performance of stocks and bonds and plan on that, but sometimes there are long stretches when returns don't look anything like long-term averages (see: the past decade). Meanwhile, some investors, particularly those that plan on consistently beating the rest of the market by a wide margin, may find out that they aren't as savvy as they thought they were.

For those that are lackadaisical when it comes to contributions, a whiff on actual returns can be disastrous. If our savvy investor above misses his 14%-per-year goal by just 2%, he finished with a portfolio of $744,000. Using the classic rule of living off 4% of your portfolio, that means he's living on a $30,000 annual budget in retirement rather than the planned-for $50,000. If he vastly overestimated his investment prowess and only ends up with the 8%-per-year that our second investor achieved, it's an outright catastrophe, leaving him with a portfolio of just $269,000 and a potential annual budget of less than $11,000.

Better together

Of course, there's no reason that you have to choose between making healthy contributions to your retirement account and choosing investments that will perform well over time.

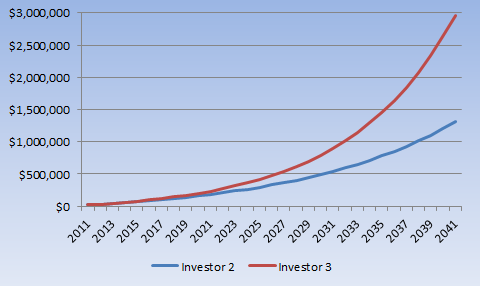

While we've already covered how the former can benefit you, the magic of compounding interest can deliver serious benefit over time if you invest wisely. Let's add a third investor to our mix. This investor has the same starting portfolio as the other two and makes the same contributions as investor No. 2. By spending some time choosing her investments, she earns 12% annual returns -- less than the 14% that investor No. 1 was gunning for, but above investor No. 2's 8%.

Here's what happens:

Over time, the higher returns for investor No. 3 make a big difference. In lifestyle terms, this could mean an earlier retirement, a more comfortable retirement, or the ability to pass an inheritance on to her children.

Those 4 stocks

Remember how I promised four stocks that would help you achieve your retirement goals? In choosing these four, my most important criterion was choosing businesses that I'm confident will continue to be successful years into the future. As my fellow Fool Morgan Housel has shown, returns over long periods of time, particularly when you reinvest dividends, can be truly astounding.

After that, my preference was for dividend-paying companies with attractive expected earnings growth and reasonable valuation multiples.

Company | Dividend Yield | Expected Long-Term Earnings Growth | Forward Price-to-Earnings Ratio |

|---|---|---|---|

IBM (NYS: IBM) | 1.8% | 12.3% | 12.0 |

CSX (NYS: CSX) | 2.4% | 15.1% | 10.9 |

Waste Management (NYS: WM) | 4.4% | 10.2% | 13.4 |

Boeing (NYS: BA) | 2.7% | 11.9% | 13.5 |

Source: Capital IQ, a Standard & Poor's company.

I guarantee that you can find more exciting stocks out there. And you'll probably end a good number of conversations talking about how you're investing in choo-choo trains (CSX) and garbage collectors (Waste Management). But you can go bungee jumping or spelunking if you want danger and excitement. If you want to retire well, start with a solid contribution plan, then look toward companies like these that have the potential to continue to earn significant profits and, as a result, line your pockets, over long periods of time.

Want some more stock ideas that are cut from the same cloth? Grab a free copy of the Motley Fool special report "13 High-Yielding Stocks to Buy Today."

At the time thisarticle was published Fool contributor Matt Koppenheffer owns shares of Waste Management, but does not have a financial interest in any of the other companies mentioned. You can check out what Matt is keeping an eye on by visiting his CAPS portfolio, or you can follow Matt on Twitter @KoppTheFool or Facebook. The Fool's disclosure policy prefers dividends over a sharp stick in the eye.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.