Is Huntington Bancshares a Buffett Stock?

As the world's third-richest person and most celebrated investor, Warren Buffett attracts a lot of attention. Thousands try to glean what they can from his thinking processes and track his investments.

While we can't know for sure whether Buffett is about to buy Huntington Bancshares (NAS: HBAN) -- he hasn't specifically mentioned anything about it to me -- we can discover whether it's the sort of stock that might interest him. Answering that question could also inform whether it's a stock that should interest us.

In his most recent 10-K, Buffett lays out the qualities he looks for in an investment. In addition to adequate size, proven management, and a reasonable valuation, he demands:

Consistent earnings power.

Good returns on equity with limited or no debt.

Management in place.

Simple, non-techno-mumbo-jumbo businesses.

Does Huntington Bancsharesmeet Buffett's standards?

1. Earnings power

Buffett is famous for betting on a sure thing. For that reason, he likes to see companies with demonstrated earnings stability.

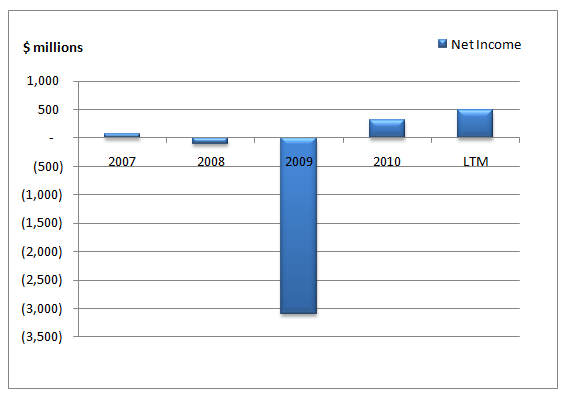

Let's examine Huntington Bancshares' earnings history:

Source: Capital IQ, a division of Standard & Poor's.

Like many other regional banks, Huntington took major losses in 2009 but is starting to rebound.

2. Return on equity and debt

Return on equity is a great metric for measuring both management's effectiveness and the strength of a company's competitive advantage or disadvantage -- a classic Buffett consideration. When considering return on equity, it's important to make sure a company doesn't have an enormous debt burden, because that will skew your calculations and make the company look much more efficient than it actually is.

Since competitive strength is a comparison between peers, and various industries have different levels of profitability and require different levels of debt, it helps to use an industry context. I'll be using a leverage ratio defined as assets divided by equity, which is more appropriate for banks. In the United States, about 10 to 12 times is considered normal.

Company | Leverage Ratio | Return on Equity (LTM) | Return on Equity (5-year average) |

|---|---|---|---|

Huntington Bancshares | 10.1 | 9% | (5%) |

Regions Financial (NYS: RF) | 7.8 | 1% | (5%) |

KeyCorp (NYS: KEY) | 9.1 | 10% | 2% |

Fifth Third Bancorp (NAS: FITB) | 8.8 | 9% | 3% |

Source: Capital IQ, a division of Standard & Poor's.

Huntington Bancshares generated a reasonable return on equity over the past five years while employing a moderate amount of leverage.

3. Management

CEO Stephen Steinour has only been at the job since 2009, but he's been in the industry for a couple of decades at places like Citizens Bancorp. He's also had a stint at the Treasury and FDIC.

4. Business

At its most complex, finance can resemble some combination of brain surgery and rocket science. With the exception of his sweetened Goldman Sachs and Bank of America deals, Buffett tends to favor somewhat simpler national banks like Wells Fargo. Huntington may not be as complicated as some of the crazier national banks, but it did get in over its head during the mortgage boom.

The Foolish conclusion

Regardless of whether Buffett would ever buy Huntington Bancshares, we've learned that the company exhibits moderate debt levels and a reasonable return on equity. Buffett might like to see a bit more of how the turnaround at Huntington plays out, though Steinour's turnaround seems to be going well so far.

If you'd like to stay up to speed on the top news and analysis on Huntington Bancshares or any other stock, simply add it to your stock watchlist. If you don't have one yet, click here to create a free, personalized watchlist of your favorite stocks.

At the time thisarticle was published Ilan Moscovitzdoesn't own shares of any company mentioned. You can follow him on Twitter@TMFDada. The Motley Fool owns shares of KeyCorp, Bank of America, Fifth Third Bancorp, and Huntington Bancshares. The Fool owns shares of and has created a ratio put spread position on Wells Fargo. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.