Silver Linings in Tomorrow's Recession

While you lounged over Labor Day, Europe had a bit of blowout. Interest rates across the continent surged yesterday. Stocks fell over 5%, with bank shares obliterated. It's starting to smell like 2008 over there.

It's only comparatively better here at home. Friday's jobs report reminded us that if you're out of a job, it's hell. No jobs were created last month, and year-to-date job creation has barely kept up with population growth. Other indicators of economic output point to a looming recession -- if, that is, you believe the last one ever ended.

But before you go out and collect two of every animal, take heart. There's good reason to think that this is not 2008 for the U.S. economy. Here are four reasons why.

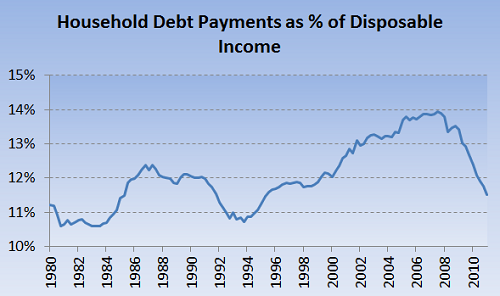

1) Household debt payments are dramatically lower.

Between debt being paid off, written off, or refinanced, household debt payments as a percentage of income have fallen dramatically since 2008, and are now actually below the long-term average:

Source: Federal Reserve.

This deleveraging is exactly what needed to happen; too much debt was the root cause of the collapse. The problem is that consumers can change their spending behavior far faster than most businesses can adapt to it. Households shifted cash to deleveraging in a heartbeat, while businesses were still built for a consumer that had a religious propensity to spend. Thus, it hurt.

The best way to quantify that retrenchment is the personal savings rate. When the recession hit, the savings rate went from 1% to 7.5%. In an economy with over $11 trillion of disposable income, that adjustment was incredible -- over $600 billion a year that used to go to consumption was suddenly being saved or used to pay down debt. And it happened virtually overnight.

The good news today is that the urge to pay off debt isn't as dire as it was in 2008. Debt levels are far more manageable. And today's personal savings rate is already a respectable 5%. Sure, it could go higher, shifting more money from consumption into savings. But it's far easier for households to go from a 1% savings rate to a 5% savings rate than it is a 5% to 9%. For many, the former requires cutting out frills, while the latter requires digging into necessities. A new recession is unlikely to bring anywhere near the kind of spending retrenchment we saw in 2008.

2. Homes prices are far closer to normal.

The bursting of a housing bubble is particularly brutal on Americans for two reasons: Regardless of income, housing is most people's largest asset, and it's usually leveraged several times over. Total household net worth in the most recent quarter was still $6 trillion below 2007 levels, with effectively all the decline coming from housing.

The good news is that prices are now far closer to normal. In fact, nationwide price-to-income ratios are now actually below historic averages:

Sources: S&P Case-Shiller, Census Bureau, and author's calculations.

Prices could go much lower, of course. And I think they will. Things don't simply revert to normal after a bubble bursts. They fall below normal and sit there for years.

But the worst of the housing collapse is almost certainly behind us. From 2007 prices, a 40% drop was practically certain. From today's prices, it would be virtually unprecedented. More specifically, homebuilders in 2007 were adding hundreds of thousands of housing units that far outstripped long-term demand. Today, it's the opposite. Some 1.5 million households will be formed per year over the next decade, yet housing construction is skidding along at less than 600,000 units a year. Excess inventory is being sucked up fast -- faster than I think most realize.

3. Companies are leaner.

Both corporate profits and corporate revenue are at all-time highs, even as unemployment is at a generational high. There are all kinds of theories explaining this, but the most convincing (and most obvious) is the idea that many of those laid off either held redundant positions within a company, or were responsible for tasks that could be passed off to another employee. It was a rush toward efficiency: Businesses could lay off millions of workers while actually juicing the bottom line.

There's evidence that that efficiency campaign has reached its limit. After surging throughout 2009 and much of 2010, productivity (output per hour worked) has seen it s growth rate collapse to less than 1%. There are far fewer low-hanging-fruit employees to be laid off today than there were in 2008. Tellingly, planned layoffs are now at the lowest level since 2000, according to Challenger, Gray & Christmas.

4. Expectations are already low.

Recessions are mainly about resetting expectations. Investors who are too bullish need to be grounded. Consumers who are too confident need to be brought to earth. Businesses that are too optimistic need a dose of reality. Recessions keep expectations in check.

But expectations are already incredibly low today. Consumer confidence is near the lowest it's been in a half century. Small business confidence is the lowest it's been in a quarter century, save for the depths of 2009. At 2%, the yield on 10-year Treasury bonds is essentially forecasting a lost decade. Several high-quality stocks, including Intel (NAS: INTC) , Microsoft (NYS: MSFT) , and ExxonMobil (NYS: XOM) trade for well under 10 times earnings. Other incredibly high-quality companies like Apple (NYS: AAPL) and Google (NAS: GOOG) aren't far behind. The biggest bull market in America is in bank deposits. That's hardly a sign of exuberance waiting to be popped. Quite the opposite, some would say.

Chin up.

There are risks, particularly when one realizes that the standard tools for fighting recessions are now virtually off limits. But economies recover from excess when, and only when, there's pain. Thankfully, there's already been a lot of that over the past three years.

At the time thisarticle was published Fool contributorMorgan Houselowns shares of Intel, Microsoft, and Exxon. Follow him on Twitter @TMFHousel. The Motley Fool owns shares of Microsoft, Google, and Apple. The Fool owns shares of and has bought calls on Intel. Motley Fool newsletter services have recommended buying shares of Apple, Microsoft, Google, and Intel. Motley Fool newsletter services have recommended creating a bull call spread position in Apple and Microsoft, as well as a diagonal call position in Intel. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insights makes us better investors. The Motley Fool'sdisclosure policyalways keeps its chin up.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.