The Economy, Viewed as It Should Be

Two years after the recession officially ended, and it still stinks.

Economic growth is slow. Jobs growth is virtually nonexistent. Consumer confidence is pitiful. If it feels like the recession never ended, it probably didn't.

Or scratch that. Maybe the past few years have been great to you. You've been gainfully employed and would have no problem finding a new job should you lose your current one.

It's actually that way for a lot of people. Economic data are reported in nationwide averages, but things get interesting when you break them out by different groups.

Take unemployment. Broken up by education level, the unemployment rate varies by a factor of four:

Source: Bureau of Labor Statistics, author's calculations.

If you don't have a high school diploma, the past three years have been wretched: Unemployment has risen from 6.9% in 2007 to 15%. Even those with some college education have been hit hard, with unemployment rising from 3.5% to over 8%. For both groups, today is recessionary by any definition.

But for those with a bachelor's degree or higher, it's relatively calm. The unemployment rate, 4.3%, is higher than it was three years ago, but only by two percentage points. Even in boom times, the overall unemployment rate is rarely as low as it is today for those with a college degree.

The same skew shows up when unemployment is broken out by age:

Source: Bureau of Labor Statistics, author's calculations.

For those in their prime working years -- age 35 and over -- today's unemployment rate is around 7%. It's the younger generation that really skews things higher. For those under age 24 (and that's really 18-24, since those in high school or younger by and large are not in the labor force), the unemployment rate is well over 20%. And since the U.S. has a fairly young population, that group does skew the national average higher.

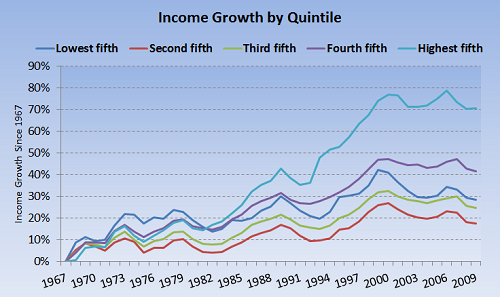

And then there's income. Nearly all Americans have seen their real incomes rise over the past 40 years:

Source: Bureau of Economic Analysis, author's calculations.

What I find interesting about this is how even it is across groups. Yes, the highest quintile of American earners have seen their income grow faster than everyone else's, but that should be expected. More productive people will always earn more, and figure out how to grow those earnings faster than others.

But each quintile's real incomes have fallen or stagnated over the past 10 years. You don't see real income growth over the past decade until you look at the top 1% of wage earners, whose earnings have risen dramatically.

Why have incomes stagnated for so many Americans? There are an untold number of theories. One that I think plays a bigger role than most appreciate is a cyclical phenomenon where economies value capital and labor at different rates.

For most of the 1950s, '60s, and '70s, having the ability to work was all you needed to get ahead. Real wages, as I've noted before, grew faster than the stock market.

That began shifting in the 1980s, when the economy began valuing capital at much higher rates. Today, substantially all of the economy's income growth goes to the top sliver of Americans. And that sliver overwhelmingly derives their income from dividends, capital gains, and interest. From capital, in other words, not labor.

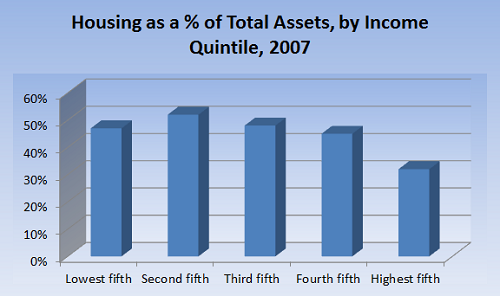

This last one, too, is interesting in how uniform it is across all income groups:

Source: Federal Reserve, author's calculations.

This chart, better than perhaps any other, helps explain why our economy as a whole is soured.

No matter how rich or poor you are, housing likely made up a large percentage of your assets in 2007. With home prices down between 10% and 60% since then (depending on region), households across the board -- essentially regardless of income -- have been devastated.

Add in the leverage that typically accompanies homeownership, and I think a more relevant question than "Why is the economy still so bad?" is "Oh my gosh, how is it not so much worse than it is?"

At the time thisarticle was published Fool contributorMorgan Houseldoesn't own shares in any companies mentioned in this article. Follow him on Twitter @TMFHousel.Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.