Time to Buy? A Closer Look at Stocks

Oscar Wilde once talked about the person who "knows the price of everything and the value of nothing."

After one of the most volatile months in modern history, investors are all too aware of the price of stocks. Their value, however, is another matter.

The history of markets is that of expensive markets becoming more expensive, and vice versa. Stocks spend very little time at the "average" that underpins most analysts' assumptions, creating a weird world where those who are probably right appear wrong most of the time. Accordingly, there will never be agreement on what the market is worth. But a couple of points might help guide your thinking.

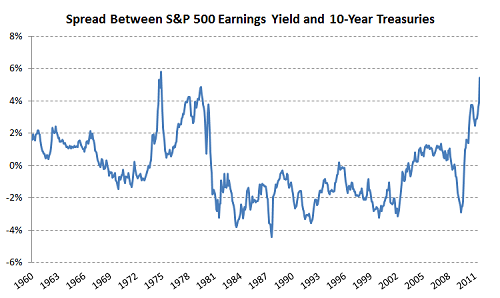

The first is the spread between the earnings yield on the S&P 500 and 10-year Treasury bonds. The idea here is that stocks and bonds compete for investors' attention, so there should be a correlation between the two. The two assets have different characteristics -- stocks are perpetual; bonds have a terminal date -- but investors can be persuaded to ditch one in favor of the other if the price is right.

After the recent market turmoil, the spread between stock earnings and bond interest is now close to a 50-year high:

Sources: Yale University, author's calculations.

In clearer terms, the earnings yield on the S&P 500 is 7.5%, while a 10-year Treasury bond yields 2.1%. The 5.4-percentage-point difference is the widest gap since the early 1970s. Stocks, in other words, yield more than bonds by the largest amount in 40 years.

Whenever there's a big outlier like that, you should ask what the market is trying to say.

Current record-low bond yields hint at dismal economic growth, if not outright deflation. But on the contrary, stock earnings have been holding up remarkably well (so far). The discrepancy between the two is what's blowing open the spread. If the bond market is right, stock earnings might be poised to plunge.

An alternative explanation is that the current spread simply reflects panic. Record-low bond yields might not forecast slow growth as much as investors' determination to avoid the volatility of stocks while seeking the stability of bonds, returns be damned. If that's the case, it might bode well for stocks.

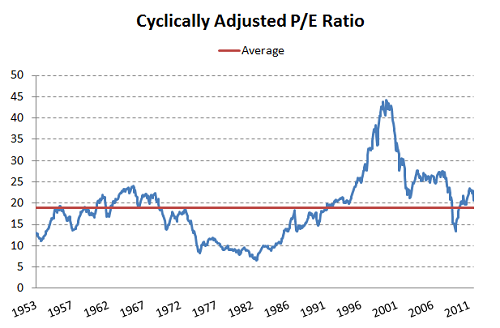

Others don't buy it. By at least one metric, stocks are still overvalued.

Yale economist Robert Shiller devised a way of valuing the market called the cyclically adjusted P/E ratio, or CAPE, which values the market with a 10-year average of earnings adjusted for inflation, which smooths out the noise of business cycles.

Since the 1950s (when the modern S&P 500 index was born), CAPE has averaged 19. Today it's at 19.5.

Sources: Yale University, author's calculations.

CAPE is hardly perfect. But it's probably the most no-bull way to value the market, immune to both forward-looking projections and short-term distortions caused by booms and busts. Benjamin Graham, Warren Buffett's early mentor, was one of the first to advise using a CAPE-like metric to value stocks. Doing so can be "useful for ironing out the frequent ups and downs of the business cycle," and can "give a better idea of the company's earnings power than the results of the latest year alone," he wrote.

By that logic, stocks might still be slightly overvalued at current prices. That doesn't mean they can't rally from here, but it gives ammo to those arguing that future returns might be meek at best.

What now?

None of this should suggest that you either go hog wild with, or bail out on, stocks. Instead, current valuations, far from being obviously cheap or obviously overvalued, stress the importance of smart stock picking.

While broad market indices might look questionable, average valuations on high-quality large-cap stocks provide opportunities for what look like reasonable bets. The average S&P 500 company trades at nearly 15 times earnings, yet for the 80 largest names, the average is less than 12 times earnings. This underscores something we've been banging on about for the past two years: If there's value in today's market, it's in high-quality giants -- names like Microsoft (NAS: MSFT) , Johnson & Johnson (NYS: JNJ) , Intel (NAS: INTC) , and Wal-Mart (NYS: WFMT) . All are above-average companies selling for below-average valuations.

Ah, value! So much more useful to discuss than price.

For more ideas on cheap, high-quality companies, check out The Motley Fool's free report 13 High-Yielding Stocks to Buy Today. Just click here. It's free.

Check back every Tuesday and Friday for Morgan Housel's columns on finance and economics.

At the time thisarticle was published Fool contributorMorgan Houselowns shares of Microsoft, J&J, Intel, and Wal-Mart. Follow him on Twitter @TMFHousel.The Motley Fool owns shares of Wal-Mart Stores, Johnson & Johnson, and Microsoft. The Fool owns shares of and has bought calls on Intel. Motley Fool newsletter services have recommended buying shares of Microsoft, Johnson & Johnson, Intel, and Wal-Mart Stores. Motley Fool newsletter services have recommended creating a diagonal call position in Johnson & Johnson.Motley Fool newsletter services have recommended creating a diagonal call position in Intel. Motley Fool newsletter services have recommended creating a diagonal call position in Wal-Mart Stores. Motley Fool newsletter services have recommended creating a bull call spread position in Microsoft. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.