The Little Known Secret of the Stock Market

Earlier this week I watched Jon Stewart interview CNN's Ali Velshi on The Daily Show and was a little surprised at something Velshi said. When explaining why the market was behaving like some out-of-control Six Flags roller coaster, Velshi said that "the stock market has become a barometer of how investors around the world feel." Stewart responded by suggesting that it's like an investor mood ring, and everyone had a good chuckle.

Velshi is a sharp guy and is CNN's chief business correspondent. And of course he's absolutely right about the stock market being a barometer for how investors feel. But I'm going to quibble with one small part of what he said, and that's that it "has bec ome a barometer."

In fact, this is nothing new at all. In his classic Security Analysis -- which was first published in 1934 -- Ben Graham wrote:

The prices of common stocks are not carefully thought out computations, but the resultants of a welter of human reactions. The stock market is a voting machine rather than a weighing machine. It responds to factual data not directly, but only as they affect the decisions of buyers and sellers.

Or we can look to Warren Buffett, who, in a 1987 letter to Berkshire Hathaway (NYS: BRK.A) (NYS: BRK.B) shareholders, quoted a similar Graham view:

As Ben said: "In the short run, the market is a voting machine but in the long run it is a weighing machine."

It's easy to lament the turbulent times that we live in and assume that things were different in "the good old days," but in this case, as in so many others, the simple ways of those times passed never really existed. Mr. Market has always been pretty nutty and investors have always allowed themselves to be pushed around by a wide array of cognitive biases.

Investors beware

Going back to Velshi, he nailed it when he told Stewart that "the stock market is a collection of the value of the underlying companies, and that's what the judgment should be." He added that the value of those underlying companies didn't change nearly as much as the stock market was suggesting last week. The latter point is something it doesn't take a PhD in finance to figure out, and yet it's something that seems so painfully overlooked sometimes.

Check out a few of the big movers last week.

Company | Price Change Aug. 5 to Aug. 8 | Price Change Aug. 8 to Aug. 9 | Price Change Aug. 9 to Aug.10 | Price Change Aug. 10 to Aug. 11 |

|---|---|---|---|---|

Berkshire Hathaway (BRK-A) | (5.9%) | 8% | (6.1%) | 4.5% |

Schlumberger (NYS: SLB) | (8.9%) | 5.4% | (4.9%) | 5% |

Citigroup (NYS: C) | (16.4%) | 13.8% | (10.5%) | 6.3% |

Source: Capital IQ, a Standard & Poor's company.

These aren't little dinghies that can be pushed around by a light wind -- these are massive companies. For a nearly $180 billion company like Berkshire Hathaway, the 8% change that it saw last Tuesday means a difference of $14.2 billion. Sure, you could argue that Berkshire owns a hefty stock portfolio that was probably getting pushed around, but we'd then want to take that a step further and ask how much the underlying value of major holdings like Coca-Cola, American Express, and Procter & Gamble (NYS: PG) were really changing in the course of one day.

Similarly, Schlumberger and Citi had some economic sands shifting under their feet, but the size and the whipsawing of those stock movements makes no sense when you start thinking in terms of the true, underlying value of the company -- not just the trading price of the paper stock.

The real smartest guys in the room

In the fall 1984 edition of the Columbia Business School magazine Hermes, Warren Buffett wrote a piece called "The Superinvestors of Graham-and-Doddsville." In it, he presented a list of long-term investment records that included his own investment partnership, Bill Ruane's Sequoia Fund, Walter Schloss' investment partnership, and Tweedy, Browne. These investors all topped the results of the broader market and did it by focusing on the underlying value of the businesses they were investing in and only buying when the wild swings of the market offered up a price that was a discount to that underlying value.

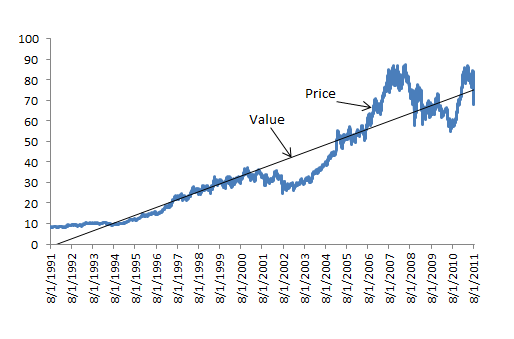

Here's a simple illustration of what we're talking about here.

The above is an actual stock chart with a trend line added. The idea is that, over time, this company has built its business and grown, and the underlying value of the business has increased. All the while, the stock market has been doing its own thing -- at times accurately recognizing what the business is worth, but often getting overly pessimistic or wildly excited and pricing the stock too high or too low.

In practice, it's not quite that easy as that, because the underlying value of a company rarely moves in a perfectly straight line. But the idea is the same -- that there is a true value for the company that usually changes slowly over time and is not necessarily reflected by the stock price.

Though the market's volatility has settled down since last week's craziness, that doesn't mean that investors are suddenly focusing on underlying value or that stocks are now priced properly. Investor pessimism and a current distaste for large-cap companies means that there are more quality companies trading at single-digit price-to-earnings multiples than we've seen in a long time. Microsoft (NAS: MSFT) and its forward P/E of 8.6 is one of my current favorites, but there are plenty of others that jump out as potential price-is-less-than-value opportunities, including Travelers Companies (NYS: TRV) and Kohl's, with respective P/E's of 8.3 and 9.5.

Want even more ideas? My fellow Foolish analysts have compiled a free report -- "13 High-Yielding Stocks to Buy Today" -- which details some of their favorite dividend-paying stocks.

At the time thisarticle was published The Motley Fool owns shares of Coca-Cola, Microsoft, Berkshire Hathaway, Citigroup, and Schlumberger.Motley Fool newsletter serviceshave recommended buying shares of Coca-Cola, Microsoft, Berkshire Hathaway, and Procter & Gamble.Motley Fool newsletter serviceshave recommended creating a bull call spread position in Microsoft. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors.Fool contributorMatt Koppenhefferowns shares of Microsoft and Berkshire Hathaway, but does not have a financial interest in any of the other companies mentioned. You can check out what Matt is keeping an eye on by visiting hisCAPS portfolio, or you can follow Matt on Twitter@KoppTheFoolorFacebook. The Fool'sdisclosure policyprefers dividends over a sharp stick in the eye.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.