Buy This Chinese Dot-Com Video Service

It looks like those rumors of Baidu (NAS: BIDU) scooping up Chinese online video streaming service Tudou (NAS: TUDO) before it went public failed to materialize.

Yesterday, shares of Tudou hit the ground moonwalking as the stock -- gasp -- closed lower! Tudou's stumble is the first Chinese Internet IPO in recent memory that hasn't soared its first day. The offering priced at $29, yet shares closed at $25.56.

According to Analysys International, as of Q1 2011, three companies command more than half of China's online video revenue. Youku.com (NYS: YOKU) took the biggest share at 21.5%, Tudou garnered 16.2%, and Sohu.com (NAS: SOHU) trailed at 13.1%. This compares with market shares of 17.7%, 12.8%, and 11.2%, respectively, for Q1 2010. All three companies have enjoyed growing market share, though recent Q2 figures showed Tudou falling back to 14% market share, while Sohu and Youku kept up their gains.

How do these three companies stack up against each other? Let's see.

Tudou

Tudou's videos consist of user-generated content, premium licensed content, and content developed in-house. As of the most recent quarter, the company boasts 90.1 million registered users, approximately 47,000 average daily new videos, and 200 million monthly unique visitors. The company has improved its advertiser retention rates from 52% in 2008 to 59% in 2010.

Revenue is at its highest level in the company's history, but unfortunately it is unable to turn a profit. Some of the recent quarterly losses are just plain mind-boggling.

Source: Prospectus.

The massive losses are tied to recent spikes in operating expenses, partially attributed to the company increasing its sales force by more than 40% over the past year. Share-based compensation expenses have also been rising precipitously. There's not much to see when it comes to Tudou, except maybe the company's in-house original drama series, That Love Comes, which now even airs with English subtitles.

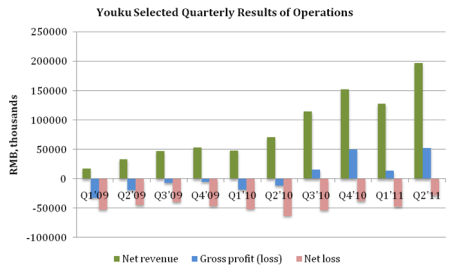

Youku.com

In contrast to Tudou, most of Youku's content is professionally produced, including more than 1,500 serial drama titles and 2,100 movie titles. According to iResearch, Youku's monthly unique visitors lead at 283 million, including visitors using Internet cafes. The market leader also has higher advertiser retention rates, topping 60% and 70% for the past two years, respectively.

The company recently reported earnings, narrowing its loss on triple-digit revenue growth. Like its second-place peer, Youku has also failed to convert this explosive revenue growth into black ink.

Source: Prospectus, second quarter 6-K.

Youku's trend is on a much better track than Tudou's, and it even seems conceivable that there's a profitable light at the end of the tunnel. The main thing that prevents me from even considering it for investment is its absurd valuation.

The company's market capitalization exceeds $3 billion as of this writing, not to mention when it was trading near $70 a few short months ago. If we were talking about a $1 billion company, I might be interested. At $3 billion, no way. Reports have just surfaced that Tencent Holdings may be in talks to buy a stake in the company, which is likely to fan the flames further.

Sohu.com

Sohu's operations are more diverse than the other video streamers. Its offerings range from massively multiplayer online role-playing games, or MMORPGs, to wireless businesses. While the company's core business remains its advertising traffic, Sohu's online video revenue increased by more than 150% last quarter, making it the company's fastest-growing area.

To put Youku's insane market cap into perspective, Youku's quarterly revenue was $50.4 million compared to Sohu's $198.7 million, and Sohu's market cap is roughly $2.8 billion -- smaller than Youku's. This puts Youku's price/sales ratio at 33.09 compared to Sohu's 4.11 and Tudou's 13.78. Sohu also has much healthier signs of profitability over the same time frames. And by healthier, I mean existent.

Source: 2010 10-K annual report, second-quarter 10-Q.

In fairness, Sohu has been around a bit longer than its younger, unprofitable competitors, so it has had time to overcome the growing pains of net losses and disproportionally high marketing expenses.

And the winner is ... Sohu!

When it comes down to the ultimate question of which of these dot-coms may deserve your dollars, my vote is with Sohu. While it sits in third place in strictly online video revenue compared to the other two, it is still exhibiting strong growth and profitability. It has more diversified operations, as well as a much more reasonable valuation. I even like it more than fellow Chinese portal site and official Fool recommendation SINA (NAS: SINA) , partially because I have doubts on its ability to monetize Weibo.

It looks like the market is off to another wild ride, which might give you a chance to pick up Sohu shares on the cheap. I'll be keeping an eye on these companies. Join me by clicking on the following links to add the stocks to your free, personalized Fool watchlist.

Add Youku.com to My Watchlist.

Add Tudou Holdings to My Watchlist.

Add Sohu.com to My Watchlist.

Add SINA to My Watchlist.

Add Baidu to My Watchlist.

At the time thisarticle was published Fool contributorEvan Niuholds no position in any company mentioned.Click hereto see his holdings and a short bio.Motley Fool newsletter serviceshave recommended buying shares of Sohu.com, SINA, and Baidu. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.