No Such Thing as a U.S. Stock Market

Find someone who's bearish on the U.S. stock market. Ask them why they're bearish. Odds are you'll hear something along the lines of, "America's economy is a mess. Washington politicians don't get it. The Fed is destroying the dollar. This country just isn't what it used to be."

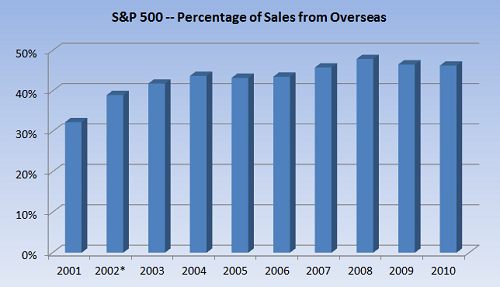

All potentially valid points. But using these arguments to justify abandoning U.S. stocks and U.S. large-cap indexes such as the S&P 500 misses something critical: Most large American corporations do a tremendous amount of business overseas. Over 46% of the S&P 500's revenue is derived outside of the United States. There's no such thing as a U.S. stock market. Companies might be listed in the U.S., but it's a global marketplace.

This trend has grown over the past decade. While leveling off in recent years, S&P 500 foreign sales as a percentage of total sales are up over 40% since 2001:

Source: Standard & Poor's. *Estimate.

Some names that are considered American icons actually do very little business in America. Intel (NAS: INTC) does 85% of sales abroad. ExxonMobil (NYS: XOM) does 66% of its business overseas. Coca-Cola (NYS: KO) is 73%. Sixteen companies in the S&P 500 do over 85% of their business outside the U.S. Just 56 do less than 15% of their business overseas.

Four sectors make up the bulk of international sales: technology, industrials, health care, and consumer discretionary. Some of the shifts over the past few years have been extreme. As a percentage of S&P 500 foreign sales, energy has fallen by half and health care has doubled since 2003:

Sector | % of 2010 Foreign Sales | % of 2003 Foreign Sales |

|---|---|---|

Consumer discretionary | 14.1% | 17.7% |

Consumer staples | 7.8% | 6.6% |

Energy | 7.8% | 18.2% |

Financials | 7.5% | 6.7% |

Health care | 12.5% | 6.2% |

Industrials | 17.3% | 17.8% |

Technology | 22.4% | 19.7% |

Materials | 9.8% | 6.6% |

Telecom | 0.4% | 0.0% |

Utilities | 0.4% | 0.5% |

Source: Standard & Poor's.

But enough tables. What does this all mean for your investments?

It changes growth prospects

Bob Doll of BlackRock estimates 70% of S&P 500 earnings growth will come from abroad over the next five years. That's a staggering figure that completely alters the investment outlook of many companies. What happens to unemployment in the U.S., or whether the U.S. housing market picks up, or whether U.S. consumer spending revives, is far less important to some companies than people think. Wal-Mart (NYS: WMT) , for example, has been chided by analysts and investors over the past two years as same-store sales in the U.S. disappoint. But brushed aside as almost irrelevant is that Wal-Mart's international growth has been phenomenal -- so strong, in fact, that earnings per share are up 75% since 2007. By focusing relentlessly on the poor performance of Wal-Mart's domestic sales, many have missed what's actually been a stellar overall growth story.

But not always in a good way

But there's another side of the international story. While overseas exposure will be a plus for the S&P 500 in coming years, there's no guarantee it will stay that way, and at the individual company level, overseas exposure can be a bane.

Americans are so painfully aware of -- or at least constantly told -- how bad the U.S. economy is that some mistakenly assume that everyone else is doing better. That's hardly the case. For companies with heavy exposure to Europe, for example, international sales may indeed be a drag on overall results. Banks like JPMorgan Chase (NYS: JPM) have deep ties in Europe that have turned into liabilities as the continent's financial system shudders.

By no means is it always a negative -- regions such as China and Brazil have been growing briskly -- but investors shouldn't always look at international exposure as necessarily growth exposure, particularly at the individual company level, where sales may skew toward a region or country in far worse shape than the United States. I like to view international exposure as simple diversification. Sometimes it will be a boost, sometimes it will be a bust. What's important is that your eggs aren't in one geographic basket.

How does international exposure factor into your investment decisions? Sound off in the comments section below.

At the time thisarticle was published Fool contributorMorgan Houselowns shares of Wal-Mart, Exxon, and Intel. Follow him on Twitter @TMFHousel.The Motley Fool owns shares of Wal-Mart Stores, JPMorgan Chase, and Coca-Cola. The Fool owns shares of and has bought calls on Intel. Motley Fool newsletter services have recommended buying shares of Wal-Mart Stores, Coca-Cola, and Intel. Motley Fool newsletter services have recommended creating a diagonal call position in Intel. Motley Fool newsletter services have recommended creating a diagonal call position in Wal-Mart Stores. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.