Exclusive: Setting the Record Straight on Great Panther Silver, Part 1

Every once in a while, on those special occasions when you know with every fiber of your being that you have information or perspective that can help protect people from making poor decisions, it may be permissible to turn up the volume just a hair.

You won't hear me shout, but I do intend to ensure that my voice is heard on this particular day.

The degree of conviction I bring reminds me of a day -- nearly three years ago -- when I raised the volume a bit to highlight the unfathomable bargain that was Silver Wheaton (NYS: SLW) at $2.51 per share. That stock has since become a powerful 15-bagger, and is one of the most efficiently profitable companies in the world. Because helping folks to successfully navigate this secular bull market for precious metals remains my primary inspiration, over the past several years I have sounded my barbaric yawp every time a chorus of premature top-callers have sought to scare investors away from these ultimate safe haven assets: gold and silver.

The real story in full voice

On this particular occasion, I raise my writer's voice to defend the good name of Great Panther Silver (ASE: GPL) . A sharply negative blog post appeared Tuesday, leveling a number of allegations and insinuations that I will challenge directly in Part 2 of this discussion. But first, the investment world deserves a far more complete summary of the miner's underlying story.

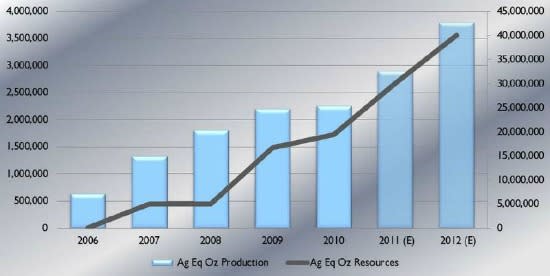

2011 marks the sixth consecutive year that Great Panther Silver will achieve year-over-year increases in production volume from its profitable pair of mining operations in Mexico. After growing output by an impressive 245% between 2006 and 2009, the company embarked upon an aggressive three-year plan to expand production by another 72% to 3.8 million silver-equivalent ounces by 2012. Over the same period, Great Panther expects to double its mineral resources to more than 40 million silver-equivalent ounces to secure at least a 10-year mine life for both operations.

Simultaneous growth trajectory for Great Panther Silver's annual output (data at left) and resource base (data at right).

Because I know from experience that the mining industry's most effective enhancements of shareholder value often come at the tip of an exploration drill, I pay close attention to the long-term resource expansion prospects at a project like Guanajuato. This mine complex sits at the heart of one of the world's premier silver and gold epithermal vein systems. Endeavour Silver's (NYS: EXK) adjacent operation of the same name has likewise provided a pillar for that operator's noteworthy growth trajectory. Over a rich mining history spanning 450 years, the broader Veta-Madre system has yielded some 1 billion ounces of silver and 4 million ounces of gold. Just last month, Great Panther increased its land holdings in the area by 136% with the purchase of four mining concessions in the nearby La Sierra vein system that hosts AuRico Gold's (NYS: AUQ) El Cubo mine.

Of course, we wouldn't call them mines at all if extracting their treasure was easy; we'd call them vaults. From first discovery to outgoing shipment, this industry is fraught with pitfalls and unexpected detours that make temporary hiccups par for the course. The expertly managed gold producer Agnico-Eagle Mines (NYS: AEM) offers one illustrative example. Great Panther Silver happened to take two minor lumps during the second quarter of 2011, but neither one is cause for alarm.

The whole story, minor hiccups and all

The miner saw its cash costs surge to $11.84 per ounce during the period as both Topia and Guanajuato mills processed some lower grade material. The only thing constant about ore grades is that they are variable! Copper miner Taseko Mines (ASE: TGB) offered one recent reminder, and certainly major miners like Newmont Mining (NYS: NEM) are not immune. At Guanajuato, the dip in grade was exacerbated by processing of low-grade surface ore from the nearby San Ignacio property in order to assess metallurgical properties. It is worth noting, however, that Great Panther achieved a 19% sequential decline in cash costs at Guanajuato from $7.85 per ounce in the first quarter to $6.35 per ounce in the second. The increase in consolidated cash costs, therefore, relates to an acute increase at Topia principally from higher smelting costs and lower ore grades. On Tuesday, Great Panther CEO Robert Archer reiterated to me that "the rise in cost per ounce is entirely due to third-party costs, while site costs have remained the same for more than a year. Our mines are sensitive to grade, smelter costs, and to byproduct credits. If we can increase the grade at our mines to previous levels, and if lead, zinc, and gold prices continue higher, then our cost per silver ounce should decline, even as our site costs remain constant."

Meanwhile, the more obvious hiccup during Great Panther's second quarter related to the steep drop in quarterly net income caused by delays in shipments of concentrate from the Guanajuato mine. Archer explains: "The concentrates from Guanajuato are somewhat different than others such as those produced from our Topia Mine in that the former contain no base metals. While Topia produces a silver-rich lead concentrate and a zinc concentrate, both of which are sold through a metal trader to smelters in Asia, the Guanajuato concentrate is a silver-and-gold-rich pyrite concentrate. Only certain smelters will accept this type of material, and we were selling through a metal trader to an overseas smelter."

It seems many smelters around the world are operating at or near capacity at present, giving them the upper hand with respect to sourcing material, pricing, and the types of concentrates they favor. According to an unnamed gold market source familiar with the issue, gold and silver pyrites like the Guanajuato concentrate would be considered relatively "complex concentrates," and metal traders are finding them "more difficult to place" as smelters give priority to less complex materials like high-grade copper concentrates. Because of this developing situation, my source informs me, Great Panther's experience would "not be unique in this market."

I also spoke Tuesday with Hugh Clarke, vice president of corporate communications for Endeavour Silver, who went on the record to share his assessment of Great Panther's excess concentrate inventory as a "small issue" that the company is "likely to resolve over the course of the next couple of quarters." Because these two miners are competitors, I consider this vocal show of support quite remarkable. Great Panther's Bob Archer confirms: "We have worked hard to rectify the situation and have made arrangements with another Mexican producer to treat our concentrates and produce dore bars, thereby reducing the inventory to normal levels by year end. The effect of this on our financials will be temporary in that, while Q2 revenues and income were lower, Q3 and Q4 should be higher than normal."

As you can see, the real story behind Great Panther Silver is a story of steady and profitable production growth paired with an exciting long-term fundamental outlook. After raising $24 million in a well-timed bought deal financing, the small-cap miner commends a $37.7 million cash position (and no long-term debt) with which to pursue its strategic goal to acquire a third mining operation. What's more, in Part 2 of this discussion (stay tuned!), I will show why I consider that the negative piece that appeared Monday to be, in Archer's own words, "so full of holes that it makes the Titanic look airtight."

Add Great Panther Silver to My Watchlist.

Add Endeavour Silver to My Watchlist.

Add Agnico-Eagle Mines to My Watchlist.

Add Taseko Mining to My Watchlist.

Add Silver Wheaton to My Watchlist.

At the time thisarticle was published Fool contributorChristopher Barkercan be foundblogging activelyand acting Foolishly within the CAPS community under the usernameTMFSinchiruna. Hetweets. He owns shares of Agnico-Eagle Mines, AuRico Gold, Endeavour Silver, Great Panther Silver, Silver Wheaton, and Taseko Mines. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.