There's a Reason Cisco Is Cheap

This week, networking Goliath Cisco Systems (NAS: CSCO) reported fourth-quarter and full-year 2011 results that beat analyst expectations, sending shares up 16% in contrast to recent earnings-triggered selloffs. Full-year GAAP EPS declined to $1.17, compared with $1.33 a year ago, on sales of $43.2 billion. For the fourth quarter, EPS landed at $0.22, versus last year's $0.33, on $11.2 billion in revenue.

But even after the jump, the stock has still lost more than a fifth of its value this year. The company has been working to cut costs by axing employees and entire business divisions while trying to reassure investors of its market leadership.

What's a Fool to do?

Some Fools are buying because the stock looks cheap. I think there are reasons that the stock is trading at its lowest P/E in years, and those reasons prevent me from buying shares.

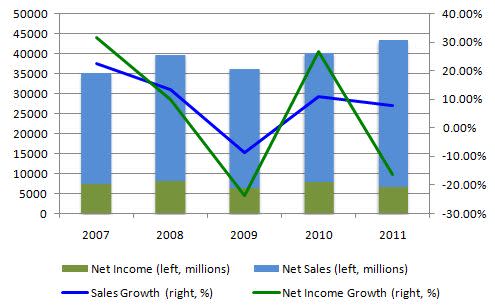

For starters, growth in revenue and earnings has been stagnant, unpredictable, and downright negative in recent years. Sales growth is one of the most important metrics to me as an investor, and Cisco isn't consistently delivering in that department.

Source: SEC filings. Figures reported on a GAAP basis.

In addition, Hewlett-Packard (NYS: HPQ) has called Cisco out for lack of innovation, which adds some context for its mixed results. After all, technology advances quickly, so you need to spend money to make money. Cisco's R&D expenditures last year came in at 13.4% of revenue, which is in line with its long-term average. If Cisco wants to prove that it's serious about the future, it needs to put its money where its mouth is and crank up the R&D.

Networking is evolving in many ways that could be opportunities for Cisco, yet it fails to capitalize in key emerging areas. F5 Networks (NAS: FFIV) has carved itself a niche in application delivery, and Riverbed Technology (NAS: RVBD) has been dominating the WAN-optimization space, despite that company's own recent revenue hiccup. Acme Packet's (NAS: APKT) session border controllers that enable delivery of interactive communications have been driving its growth.

The company's core markets, routers and switches, aren't even safe. Juniper Networks (NAS: JNPR) has been growing its share in routers, while HP gains traction in the switches market. Apple has proved that market share isn't everything if it can make up the difference in profit share, but Cisco is missing out in new markets and its bread-and-butter sectors.

A picture is worth a thousand words

The negative trend in margins paints an even grimmer picture:

Source: SEC Filings. Figures reported on a GAAP basis.

It's no surprise that this graph eerily resembles the stock's price chart over the past year. Gross margin took a big hit last year, which prompted questions from analysts during the most recent conference call. When asked whether management saw gross margin starting to stabilize, Cisco CEO John Chambers vaguely replied, 'We do not see a major falling off the cliff-type scenario on margins."

Despite the frightening imagery, the company disclosed its plans last quarter to reduce its annualized operating expense run rate by roughly $1 billion. Keep in mind that any operating cost savings won't help gross margin, since operating expenses come after gross profit on the income statement. Cost reductions would benefit operating and net margins.

Why ask why?

To get an even deeper insight into Cisco's declining performance, let's do a quick DuPont analysis to see where the company's weakness lies. This useful tool allows investors to break down return on equity into various components of performance.

Metric | 2007 | 2008 | 2009 | 2010 | 2011 |

|---|---|---|---|---|---|

Net profit margin | 21% | 20.4% | 17% | 19.4% | 15% |

Asset turnover | 0.65 | 0.67 | 0.53 | 0.49 | 0.50 |

Financial leverage | 1.69 | 1.71 | 1.76 | 1.83 | 1.84 |

Return on equity | 23.3% | 23.4% | 15.9% | 17.5% | 13.7% |

Source: SEC filings. Figures reported on a GAAP basis.

We already knew net margin was on the decline. The asset turnover ratio measures how efficiently a company uses its assets to generate sales, which in Cisco's case has been softening. The financial leverage ratio measures the amount of debt being used to finance assets. By taking on more debt over the years, Cisco increases its leverage and financial risk. The product of these metrics yields return on equity, a measure of how well the company is growing your stake in it.

It's a (value) trap!

We've seen a lot of major technological advancements over the past several years, and somehow Cisco has missed the boat. If management can turn the ship around, then this stock could be a good value purchase now. With a market cap of almost $88 billion, it's a big vessel to redirect, and I'm skeptical.

Don't buy a stock just because it looks cheap. Cisco's anemic revenue growth, declining margins, operational inefficiencies, and lack of innovation all point toward a diminishing valuation.

Add Cisco Systems to My Watchlist.

Add Riverbed Technology to My Watchlist.

Add Juniper Networks to My Watchlist.

Add Hewlett-Packard to My Watchlist.

Add F5 Networks to My Watchlist.

Add Acme Packet to My Watchlist.

At the time thisarticle was published Fool contributorEvan Niuowns shares of Riverbed Technology and Apple, but he holds no other position in any company mentioned. Check out hisholdings and a short bio. The Fool owns shares of and has created a bull call spread position on Cisco Systems.Motley Fool newsletter serviceshave recommended buying shares of Acme Packet, Cisco Systems, and Riverbed Technology. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.