Why Investors Prefer Burritos Over Big Macs

The price-to-earnings ratio tells us that investors consider Chipotle Mexican Grill's (NYS: CMG) earnings three times more valuable than McDonald's (NYS: MCD) , despite the latter's history and size. Unraveling why will help you become a better investor.

The value of earnings

The P/E ratio tells us how much we have to pay for one dollar of a company's earnings. It's calculated by dividing the price of a company's shares by its total earnings. If the company's earnings are positive, you end up with a number generally between 1 and 100.

P/E ratios in the restaurant industry range tend to fall below 50, as illustrated in the accompanying table, with most between 10 and 25.

Company | Share Price | EPS | P/E Ratio | Est. 2012 Sales Increase |

|---|---|---|---|---|

Chipotle Mexican Grill | $302.56 | $6.05 | 50.0 | 18.2% |

BJ's Restaurants (NAS: BJRI) | $42.51 | $0.97 | 43.9 | 15.2% |

Buffalo Wild Wings (NAS: BWLD) | $58.06 | $2.41 | 24.1 | 23% |

Starbucks (NAS: SBUX) | $36.04 | $1.52 | 23.7 | 10% |

Yum! Brands (NYS: YUM) | $50.34 | $2.49 | 20.2 | 5.6% |

Cheesecake Factory | $25.94 | $1.49 | 17.4 | 5.9% |

McDonald's | $85.96 | $4.94 | 17.4 | 5.7% |

Ruby Tuesday | $8.04 | $0.72 | 11.1 | 1.9% |

Wendy's | $4.76 | $0 | N/M | (6.8%) |

Source: Yahoo! Finance.

How P/E ratios and future growth rates are related

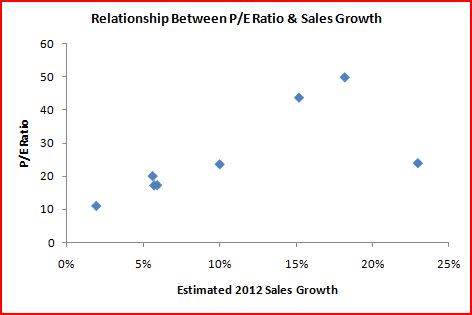

The difference between these ratios is largely a function of projected growth. Investors will pay more for a dollar of earnings today if they believe it will turn into two dollars tomorrow.

The following chart drives this fact home. Witness the strong correlation between the P/E ratios and estimated sales increases of the restaurants in the preceding table:

To bring things full circle: Investors are willing to pay three times more for Chipotle's earnings than McDonald's because Chipotle's projected growth rate is three times faster.

What the future holds

There is no question that McDonald's still has plenty of growth ahead. In China alone, McDonald's plans to increase its presence as much as tenfold, from approximately 1,000 restaurants today to between 5,000 and 10,000 in the future.

Unfortunately, it has to play catch-up in China with its principal competitor, Yum! Brands, the company behind KFC and Pizza Hut. Just last quarter, Yum! added 99 new restaurants to the nearly 4,000 it already operates in China. Starbucks, which is already challenging McDonalds in the U.S., is moving into China in a big way, too.

Chipotle, on the other hand, has the relative advantage of being small. For it to double in size -- which it's more than accomplished already in the past five years -- it would have to increase its revenue by $2 billion. Although that's hardly chump change, McDonald's would have to increase revenue by a staggering $24 billion to accomplish the same feat.

The principle that smaller can be better similarly drives the high P/E ratios of companies like BJ's Restaurants and Buffalo Wild Wings. Both operate significantly fewer restaurants than either Chipotle or McDonald's, but open new locations regularly.

Foolish takeaway

Although we've limited our discussion to the restaurant industry, the principles governing the P/E ratio apply across the market. Whenever you're considering whether to buy or sell a stock, check this ratio first to see whether it's consistent with your judgment of the company's growth prospects.

If you're interested in learning more about stocks and investing, take a look at our free reports "The Motley Fool's Top Stock for 2011."

At the time thisarticle was published Fool contributor John Maxfield does not own shares in any of the companies mentioned in this article. The Motley Fool owns shares of Yum! Brands, Starbucks, and Chipotle Mexican Grill.Motley Fool newsletter serviceshave recommended buying shares of Yum! Brands, Buffalo Wild Wings, Starbucks, McDonald's, and Chipotle Mexican Grill, and creating an iron condor position in Chipotle. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.