Amid the Market Carnage, Apple's the New King

Only a bit more than a year after it passed Microsoft (NAS: MSFT) as the most valuable company in technology, Apple (NAS: AAPL) has its sights set on a new target: the most valuable company in the world.

In the middle of the day Tuesday, Apple briefly passed ExxonMobil (NYS: XOM) to become the world's most valuable company. Afterward, Apple slipped back a bit, but make no mistake -- we witnessed the passing of the torch today.

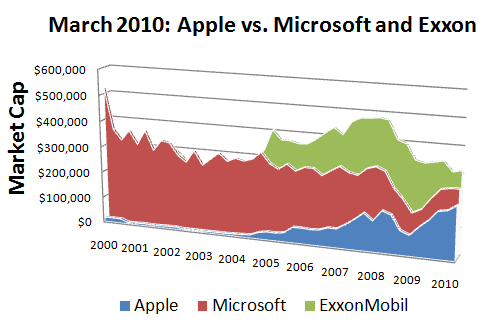

For Apple, today's news is a long way from the bottom. In late 2000, Apple was worth just short of $5 billion, while Exxon was worth more than $300 billion, and Microsoft sat at a value of more than $360 billion. Despite its explosive growth since then, Apple still would've had to grow 56% to reach ExxonMobil's size just a year and a half ago, as this chart from last March shows:

Source: Capital IQ, a division of Standard & Poor's.

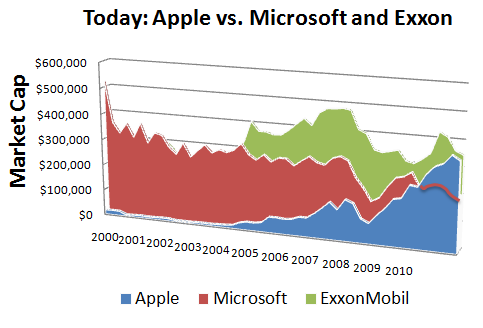

However, since then Apple hasn't just continued to sell enough iPhones, at fat enough margins, to command nearly two-thirds of all mobile phone profits. It's also released the iPad to a world skeptical of the need for what basically amounted to a larger iPhone.

The iPad doubters were wrong. As each quarter passed, and Apple obliterated estimates again and again, Wall Street proved wrong, too. Apple's stock kept soaring, while fumbling competitors like Microsoft saw their stock stagnate.

Source: CapitalIQ, a division of Standard & Poor's.

Brushing off the market carnage

The ascent of a new stock market king comes amid Wall Street panic. In the past week alone, oil fell nearly 18%, as investors feared a double-dip recession would curtail demand. That explains ExxonMobil's 12% plunge during that time. However, while it has seen its own 6% drop, Apple has hung on far better than either Exxon or the general market during the past week's panic.

That might not seem fair to investors. After all, Apple sells premium-priced products, which simple logic dictates should struggle in a double-dip recession. If investors are fretting over that very scenario, and sending markets crashing in the process, shouldn't Apple be falling more than other stocks instead of swiftly rebounding ahead of the market?

Brushing off consumer fears

No, it shouldn't. You can largely thank the unique business model of the iPhone, and smartphones in general, for that resilience. Apple sells iPhones to carriers at an average price that exceeds $650 per phone. Competitors such as HTC might sell their phones to carriers at a price around $450, but in the end, carriers subsidize both models -- meaning they effectively eat part of the cost of the phone -- and are sold at relatively similar prices. In the United States, top-end smartphones generally sell at about $200 after contract. This artificial market, where phones are subsidized and consumers generally don't realize the full cost of their purchases, allows Apple to collect those amazing profit margins on its phones.

Another economic downturn could hurt Apple's other product lines, like Macs and iPads, which aren't as heavily subsidized. It might even force consumers to reevaluate their pricey data plans. But on the whole, the iPhone's driving Apple's bottom line. It now contributes 47% of Apple's sales, and an even greater proportion of its profits. With the iPhone holding up better than expected even as the economy sputters, Apple's continuing growth looks like it's in good shape.

But wait, there's more good news!

One other area is driving Apple's results: booming international sales. That's a common trend, especially in technology; Intel (NAS: INTC) credited growth in markets like China and Brazil for its ability to crush analyst estimates last quarter.

Once again, analysts lowballed Apple's ability to succeed abroad. Consumers in these markets don't have a lot of money. In China, a new unlocked iPhone would eat up 49.7% of the average citizen's annual household income. Also, while contracts that subsidize phone costs are common in developed markets, in emerging markets it's more common for phones to be sold at their far higher actual selling price.

However, against all these obstacles, Apple has seen demand boom across the world, with the highest growth seen in developing Asian markets.

Market | Sales Growth Between 2005 and 2010 | Profit Growth Between 2005 and 2010 |

|---|---|---|

Americas | 268% | 682% |

Europe, Africa, and Middle East | 508% | 1,518% |

Japan | 331% | 1,156% |

Asia-Pacific | 727% | 2,991% |

Source: Capital IQ, a division of Standard & Poor's. Retail sales are distributed in proportion to general sales level. Accounting for regional differences in retail store sales, end sales may differ slightly.

Just last quarter alone, Apple was proud to brag that sales to Greater China had grown sixfold. Last quarter, sales to Greater China totaled a sizable $3.8 billion. Even if American and European growth fizzles off, Apple should still see continuing growth in emerging markets.

The new king to stay

So even as the market crashes around us, Apple's growth story looks surprisingly strong. While investors might be afraid to buy Apple, based on either its sheer size or their own fear that another recession could quickly sap its growth, the company's future looks surprisingly strong. Trading at just 14 times earnings, with plenty of growth ahead of it and $76 billion in the bank, Apple still looks like a compelling deal. The crown atop Steve Jobs' head appears perfectly fitted.

To keep up to date on any companies listed above, make sure to add them to our free My Watchlist service. It'll provide you with news and analysis on all your favorite companies.

Add Apple to My Watchlist.

Add ExxonMobil to My Watchlist.

Add Microsoft to My Watchlist.

Add Intel to My Watchlist.

At the time this article was published Eric Bleeker owns shares of no companies listed above. The Motley Fool owns shares of Apple and Microsoft. The Fool owns shares of and has bought calls on Intel. Motley Fool newsletter services have recommended buying shares of Intel, Microsoft, and Apple. Motley Fool newsletter services have recommended creating a bull call spread position in Apple. Motley Fool newsletter services have recommended creating a diagonal call position in Intel. Motley Fool newsletter services have recommended creating a bull call spread position in Microsoft. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.