What the Debt Deal Might Do to the Economy

Disappointment over this week's budget deal was predictable. Colin Powell once said that "being responsible sometimes means pissing people off." This bill did just that. Either it didn't cut enough, or it cut too much, or cut in the wrong areas, or it didn't include taxes, or it left the door open to new taxes. Very few are happy.

And maybe they shouldn't be. Dig into the details of the bill, and compare it with how similar spending agreements have played out in the past, and you can make sensible arguments that justify everyone's frustrations. The bill probably can't be taken seriously. It probably doesn't cut enough. And it might slow the economy while doing little to close the deficit.

Start with the first argument, that it shouldn't be taken seriously. Most of what the bill does lies not in making sacrifices today, but in vague promises between 2013 and 2023. As a rule of thumb, whenever a bill promises to do something 12 years from now, ignore it. It will almost certainly have no impact on reality. John Cassidy of The New Yorker elaborated eloquently this week:

The United States, like every other country, budgets on an annual basis. What really matters for the economy, and for the unemployed, is how much cash the federal government will spend in the remaining months of the 2011 fiscal year and in fiscal 2012, which begins October 1st. A pledge to cut spending in 2016, say, is just that: a pledge. Between now and then, we will have another bipartisan spending review (that's also part of the deal), a Presidential election, and who knows how many budget battles. The actual 2016 spending outcome will almost certainly bear little relation to the figures in this agreement.

Here's a good example. The 2002 budget agreement proposed spending $2.2 trillion in 2006. The actual number ended up being $2.6 trillion. Whoops. The 2006 plan called for $3 trillion in spending by 2010. The actual number was $3.5 trillion, with nearly all the increase coming from defense spending ($200 billion over estimates) and unemployment benefits ($230 billion over estimates). Projections of future spending are invariably inaccurate. And to the extent the current bill attempts to enforce spending cuts, remember that the debt ceiling itself is designed to enforce restraint, yet has been raised 88 times since the 1940s. Anything can be changed with a vote -- and the tough things usually are.

Even if the planned cuts do materialize, will they be enough to make a difference? It's hard to say. The bill cuts spending in two blocks: $900 billion over 10 years upfront, and between $1.2 trillion and $1.5 trillion over a decade in a deal still yet to be forged. The first $900 billion is designed to cut discretionary spending and defense spending, while leaving entitlements like Social Security and Medicare safe. The second round potentially brings entitlements into the picture, but there's no firm guarantee that it will, and every reason to believe that the bipartisan committee tasked with finding the cuts will avoid entitlement reform as much as they can. Here's their incentive: Even voters bent on austerity get prickly when you tweak their monthly checks.

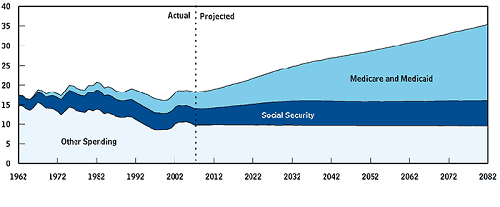

That could be a problem, as the story of our long-run deficits is about entitlement spending and basically nothing else:

Source: Congressional Budget Office. Y-axis is spending as a percentage of GDP.

Any serious long-term budget proposal would focus relentlessly on entitlements -- particularly health-care costs -- and ignore everything else, which add up to a rounding error in the grand scheme of things.

To be fair, this isn't a long-term plan. It's a 10-year plan. But just like the long run, deficits over the next 10 years are caused by one overwhelming factor: unemployment and slow economic growth.

Cutting government spending could do a number to exacerbate those problems. Consider: Over the past 18 months, the private sector has added 2 million jobs, while the government sector has shed half a million -- mostly from state and local governments that have relied heavily on federal aid.

The arithmetic for laying off government workers in the name of deficit reduction is fuzzy -- particularly when unemployment is high and those workers might remain jobless. They were paying as much as 35% in federal income taxes, and while jobless they're entitled to unemployment benefits that can equal an even larger portion of their previous pay. Both offset the savings from lower government salaries. Laying off a government worker making $60,000 a year can mean $15,000 in lost tax revenue, $25,000 in added unemployment-benefit costs, and $2,000 in added food-stamp costs. The net impact on the deficit is small. Tellingly, about half of the increase in the deficit between 2007 and today has been caused by lower tax revenue and higher unemployment-benefit costs.

Powell was right. No one's happy. They're even pissed. But was this the responsible thing to do? You tell me below.

Check back every Tuesday and Friday for Morgan Housel's columns on finance and economics.

At the time thisarticle was published Fool contributorMorgan Houseldoesn't own shares in any of the companies mentioned in this article. Follow him on Twitter @TMFHousel. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.