Is JDS Uniphase the Top Optical Innovator?

Few fields move as rapidly as technology. Businesses creating outsized profits and returns for shareholders quickly get a bull's-eye painted on their back as they become targets of other companies looking to disrupt their products by selling cheaper alternatives that still prove "good enough." Not only that, but even if a company continues to dominate its particular field, other changes in technology can shift spending away from their products. Think about how Microsoft still dominates PCs but feels pressure from the sales shift toward mobile devices such as smartphones and tablets.

With that in mind, today we're looking at how JDS Uniphase (NAS: JDSU) innovates.

Technology companies can innovate either through acquisitions or by spending more money on research and development. We'll compare JDS Uniphase's spending in these areas with that of its closest peers and assess whether the company is investing enough in its future.

Research and development

Over the past five years, JDS Uniphase has spent an average of 13% of revenues on R&D. The following table summarizes how JDS Uniphase's R&D expenditures relative to revenues compare with some of the company's closest peers and competitors.

Company | 2006 | 2007 | 2008 | 2009 | 2010 | LTM |

|---|---|---|---|---|---|---|

JDS Uniphase | 12.9% | 12.1% | 12.2% | 13.0% | 12.8% | 13.3% |

Finisar (NAS: FNSR) | 14.9% | 13.1% | 15.7% | 16.1% | 15.0% | 12.4% |

IPG Photonics (NAS: IPGP) | 4.6% | 5.0% | 6.9% | 10.0% | 6.4% | 6.0% |

Oclaro (NAS: OCLR) | 18.4% | 22.9% | 14.1% | 12.4% | 10.6% | 12.4% |

Source: Capital IQ, a division of Standard & Poor's. LTM = last 12 months. Dates above are calendar years; yearly total is for company fiscal years closing in that period.

JDS Uniphase seems to stack up well compared with its competitors in this space. Of the group, JDS Uniphase has the highest sales, which means that even if its R&D spending as a percentage of sales drops, it can still outspend rivals on an absolute basis. However, it's worth noting that the company also carries a sizeable test and measurement division, which also requires R&D resources. So total R&D spending on its larger optical-products divisions is probably not substantially larger than Finisar's, which focuses entirely on the optical subsystems market.

IPG Photonics spends far less than its competitors on R&D. That's in large part because the company's core focus is in industrial lasers, while optical subsystems are a small part of its total business. The company's R&D spending is in line with key industrial-laser rival Rofin-Sinar (NAS: RSTI) .

The important thing to remember about innovation is that although it's important to any business, keeping a tight focus and targeting the right industries is just as important, if not more so. In JDS Uniphase's case, the company became a sprawling mess during a series of jubilant dot-com mergers in which it used overvalued stock to become a one-stop optical supplier. This was a failed strategy, in large part because enthusiasm for optical networking far surpassed the need for high-speed equipment. However, in recent years JDS Uniphase has aggressively cut back, leaving itself a profitable company after a tumultuous decade that included a $56 billion loss one year after the company had to write off a string of failed acquisitions.

Although innovation will be important for JDS Uniphase in the years to come, slimming down to focus on the right areas of optical networking is what's been driving the company's turnaround.

Acquisitions

In technology, some of the best companies have turned growth through acquisitions into an art. IBM has adeptly spun off capital-heavy businesses such as the hard-drive and PC segments, while it focused on acquiring additional services and software expertise that have transformed its business model.

On the opposite end of the spectrum, Hewlett-Packard is often criticized for underinvesting in R&D, to the point that it has to overpay on acquisitions to catch up with its competitors.

Investors should remember, most of all, that companies are valued by the cash flow they can bring in for their shareholders over time. If companies need to continue making purchases in perpetuity to keep growing, that amounts to a reduction in cash flows, and investors should treat acquisition spending as a continuing outflow against cash flow.

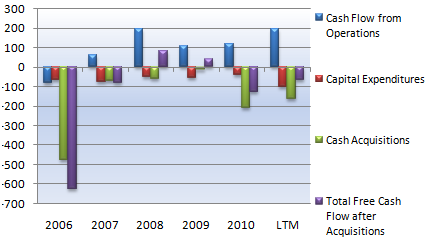

Let's take a look at JDS Uniphase's free cash flow over the past five years against cash spent on acquisitions.

Source: Capital IQ, a division of Standard & Poor's. LTM = last 12 months. Dates above are calendar years; yearly total is for company fiscal years closing in that period.

Although JDS Uniphase has (thankfully) learned quite a bit from its dot-com days and maintains much more discipline in the M&A markets today, it is still a fairly acquisitive company. Its most notable recent transaction was purchasing Agilent Technologies' (NYS: A) network solutions test business for $165 million. That's a business that folds in nicely with JDS Uniphase's existing test-and-measurement segment, and the fact that JDS Uniphase paid a reasonable 1 times sales multiple shows the maturity of its M&A strategy since the dot-com bubble popped.

Still, investors should take note that after considering cash acquisitions, the company rarely has positive free cash flow. Being a frequent acquirer doesn't exclude a company from your investing dollar, but it does raise a red flag.

Final thoughts

If you're looking to stay updated on JDS Uniphase, or any other companies mentioned here, make sure to add them to our free watchlist service, My Watchlist. It's free, and it helps you constantly stay updated on news and analysis on your favorite companies.

At the time thisarticle was published Eric Bleeker owns shares of no companies listed above. The Motley Fool owns shares of Rofin-Sinar Technologies, Microsoft, and IPG Photonics. Motley Fool newsletter services have recommended buying shares of Microsoft, Rofin-Sinar Technologies, and IPG Photonics and creating a covered collar position in Microsoft. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.