Why Varian Medical Systems May Be About to Take Off

Here at The Motley Fool, I've long cautioned investors to keep a close eye on inventory levels. It's a part of my standard diligence when searching for the market's best stocks. I think a quarterly checkup can help you spot potential problems. For many companies, products that sit on the shelves too long can become big trouble. Stale inventory may be sold for lower prices, hurting profitability. In extreme cases, it may be written off completely and sent to the shredder.

Basic guidelines

In this series, I examine inventory using a simple rule of thumb: Inventory increases ought to roughly parallel revenue increases. If inventory bloats more quickly than sales grow, this might be a sign that expected sales haven't materialized.

Is the current inventory situation at Varian Medical Systems (NYS: VAR) out of line? To figure that out, start by comparing the company's figures to those from peers and competitors:

Company | TTM Revenue Growth | TTM Inventory Growth |

|---|---|---|

Varian Medical Systems | 7.9% | 13.7% |

Hill-Rom (NYS: HRC) | 8.7% | 9.5% |

PerkinElmer (NYS: PKI) | 16.5% | (0.8%) |

Accuray (NAS: ARAY) | (4.5%) | 21.9% |

Source: Capital IQ, a division of Standard & Poor's. Data is current as of latest fully reported quarter. TTM = trailing 12 months.

How is Varian Medical Systems doing by this quick checkup? At first glance, not so great. Trailing-12-month revenue increased 7.9%, and inventory increased 13.7%. Over the sequential quarterly period, the trend looks healthy. Revenue grew 11.8%, and inventory grew 4.9%.

Advanced inventory

I don't stop my checkup there, because the type of inventory can matter even more than the overall quantity. There's even one type of inventory bulge we sometimes like to see. You can check for it by examining the quarterly filings to evaluate the different kinds of inventory: raw materials, work-in-progress inventory, and finished goods.

A company ramping up for increased demand may increase raw materials and work-in-progress inventory at a faster rate when it expects robust future growth. As such, we might consider oversized growth in those categories to offer a clue to a brighter future, and a clue that most other investors will miss. We call it "positive inventory divergence."

On the other hand, if we see a big increase in finished goods, that often means product isn't moving as well as expected, and it's time to hunker down with the filings and conference calls to find out why.

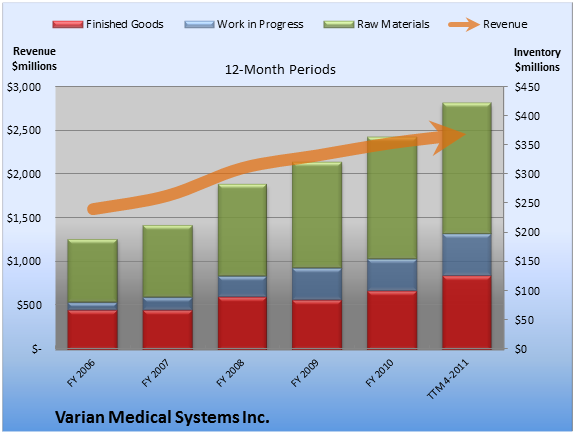

What's going on with the inventory at Varian Medical Systems? I chart the details below for both quarterly and 12-month periods.

Source: Capital IQ, a division of Standard & Poor's. Data is current as of latest fully reported quarter. Dollar amounts in millions. FY = fiscal year. TTM = trailing 12 months.

Source: Capital IQ, a division of Standard & Poor's. Data is current as of latest fully reported quarter. Dollar amounts in millions. FQ = fiscal quarter.

Let's dig into the inventory specifics. On a trailing-12-month basis, work-in-progress inventory was the fastest-growing segment, up 41.9%. On a sequential-quarter basis, raw materials inventory was the fastest-growing segment, up 6.6%. Although Varian Medical Systems shows inventory growth that outpaces revenue growth, the company may also display positive inventory divergence, suggesting that management sees increased demand on the horizon.

Foolish bottom line

When you're doing your research, remember that aggregate numbers such as inventory balances often mask situations that are more complex than they appear. Even the detailed numbers don't give us the final word. When in doubt, listen to the conference call, or contact investor relations. What at first looks like a problem may actually signal a stock that will provide the market's best returns. And what might look hunky-dory at first glance could actually be warning you to cut your losses before the rest of the Street wises up.

I run these quick inventory checks every quarter. To stay on top of the inventory story at your favorite companies, just use the handy links below to add companies to your free watchlist, and we'll deliver our latest coverage right to your inbox.

Add Varian Medical Systems to My Watchlist.

Add Hill-Rom to My Watchlist.

Add PerkinElmer to My Watchlist.

Add Accuray to My Watchlist.

At the time thisarticle was published Seth Jaysonhad no position in any company mentioned here at the time of publication. You can view his stock holdingshere. He is co-advisor ofMotley Fool Hidden Gems, which provides new small-cap ideas every month, backed by a real-money portfolio. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.