2 Nasdaq Stocks That Could Crush Nvidia and Deliver Bigger Gains, Thanks to Artificial Intelligence (AI)

The Nasdaq-100 Technology Sector index has been in fine form in the past year, clocking impressive gains of 50%, as some of the key components of this index have witnessed a red-hot rally thanks to the proliferation of artificial intelligence (AI).

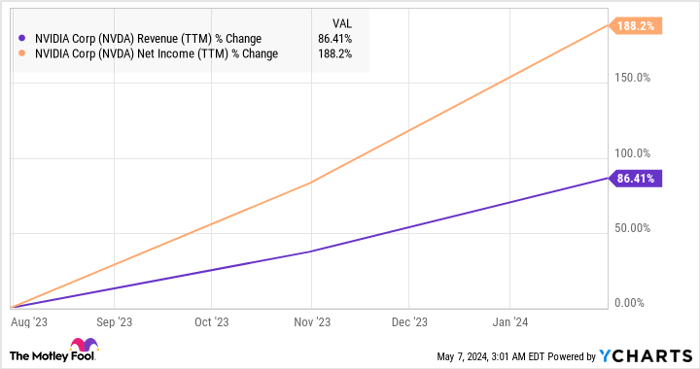

Shares of Nasdaq-100 component Nvidia (NASDAQ: NVDA), for instance, have shot up 221% in the past year. The chipmaker's terrific rally is justified by its outstanding growth. Nvidia's monopoly-like position in the market for AI chips -- where it holds 95%-plus market share according to some estimates -- has supercharged the company's top and bottom lines, which is evident from the chart below.

NVDA Revenue (TTM) data by YCharts.

What's more, analysts are expecting Nvidia's earnings to increase at a healthy annual rate of 38% over the next five years. Based on Nvidia's earnings of $12.96 per share in the recently concluded fiscal 2024, its bottom line could jump to almost $65 per share after five years, according to analyst estimates.

Even if Nvidia trades at 30 times earnings after five years, in line with the Nasdaq-100's earnings multiple, its stock price could jump to $1,950. That would be a 112% jump from current levels.

However, Nvidia isn't the only stock that's winning big from the rapid adoption of AI. There are two other Nasdaq stocks that are making the most of the AI opportunity and they could deliver more upside than Nvidia over the next five years.

1. Super Micro Computer

Super Micro Computer (NASDAQ: SMCI) stock has outperformed Nvidia in the past year with stunning gains of 505%. Supermicro, which is known for manufacturing AI server solutions, can continue to outperform Nvidia over the next five years, thanks to the fast-growing market it operates in.

Supermicro's servers are deployed by data center operators to mount chips from the likes of Nvidia and other chipmakers, which keeps their operating costs in check. Supermicro's modular server solutions aim to lower electricity and cooling costs in data centers.

For instance, Supermicro launched liquid-cooled server solutions for deploying Nvidia's massively popular H100 chips in May last year, claiming that they can reduce electricity costs in data centers by 40%. Additionally, Supermicro claims that its liquid-cooled H100 servers could reduce cooling costs by 86% when compared to existing data centers.

Considering the significant amount of electricity that AI data centers consume, the demand for Supermicro's servers is booming. This explains why the company's revenue and earnings grew remarkably in the previous quarter. Super Micro's fiscal 2024 third-quarter revenue (for the three months ended March 31) tripled year over year to $3.85 billion. Its earnings jumped fourfold to $6.65 per share.

Supermicro's full-year guidance now calls for revenue to increase 110% year over year to $14.9 billion at the midpoint. Earnings are expected to jump to $23.69 per share from $11.81 per share in the same period last year. Even better, analysts are expecting its earnings to increase at an annual rate of 62% for the next five years.

That won't be surprising as the market for AI servers is expected to clock annual growth of 30% over the next decade. Supermicro is growing faster than the market it serves, which explains why analysts are expecting its earnings growth to remain robust. Assuming the company's bottom line does grow at 60% a year for the next five years, its earnings could hit $124 per share after five years.

Multiplying the projected earnings with the Nasdaq-100's earnings multiple of 30 points toward a stock price of $3,720 after five years, a 348% jump from current levels. Even if growth rates taper off, Supermicro still has a better growth probability than Nvidia. So, Supermicro looks like a solid alternative to Nvidia for investors looking to buy an AI stock right now, given that it seems capable of outperforming the latter over the next five years.

2. Meta Platforms

Meta Platforms (NASDAQ: META) is another tech giant that's capitalizing on the adoption of AI. The social media bellwether has been integrating AI tools into its different platforms and is also leveraging the technology to help advertisers increase returns on their spending.

CEO Mark Zuckerberg explained Meta's AI initiatives in detail on the company's first-quarter earnings conference call last month. He claimed that the company's generative AI assistant, Meta AI, has been tried by "tens of millions of people," and it will be rolled out in more countries and languages in the future.

Meta AI is being integrated into WhatsApp, Facebook, Messenger, and Instagram. From allowing creators to generate high-quality images to enabling businesses to suggest products for customers, Meta Platforms is setting itself up to monetize its AI offerings in the long run. According to Zuckerberg:

On the upside, once our new AI services reach scale, we have a strong track record of monetizing them effectively. There are several ways to build a massive business here, including scaling business messaging, introducing ads or paid content into AI interactions, and enabling people to pay to use bigger AI models and access more compute. And on top of those, AI is already helping us improve app engagement which naturally leads to seeing more ads, and improving ads directly to deliver more value.

The good news for investors is that Meta's AI offerings are giving the company's growth a nice boost. Its revenue increased 27% year over year in the first quarter of 2024 to $36.4 billion. Earnings, meanwhile, shot up an impressive 114% year over year to $4.71 per share. Meta should be able to sustain a healthy earnings growth rate in the long run as it starts monetizing more of its AI offerings.

Analysts are currently expecting the company's earnings to increase at an annual rate of 28% over the next five years, which would be a nice jump over the 11% annual earnings growth it has clocked in the past five years. Using its 2023 earnings of $14.87 per share as the base, Meta's bottom line could jump to $51 per share in five years based on the potential earnings growth that analysts expect it to deliver.

Multiplying that with the Nasdaq-100's earnings multiple of 30 points toward a stock price of $1,530 after five years, a 229% jump from current levels. Given that the stock is trading at 27 times earnings right now, investors are getting a good deal on this Nasdaq stock that seems capable of outperforming Nvidia in the long run.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $550,688!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 6, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms and Nvidia. The Motley Fool has a disclosure policy.