11 Basic Money Moves Everyone Should Make During Hard Times

The coronavirus pandemic has taken a major hit on the economy and the personal finances of workers across the country. The national unemployment rate was as high as 14.7% in April 2020. It's down to 6.1% now, but many Americans are still struggling to find jobs that pay them enough to stay afloat.

Support Small: Don't Miss Out on Nominating Your Favorite Small Business To Be Featured on GOBankingRates -- Ends May 31

Whether you've lost your job, are experiencing reduced hours or are among the fortunate Americans who are still employed, here are the money moves experts say everyone should be making right now.

Last updated: May 18, 2021

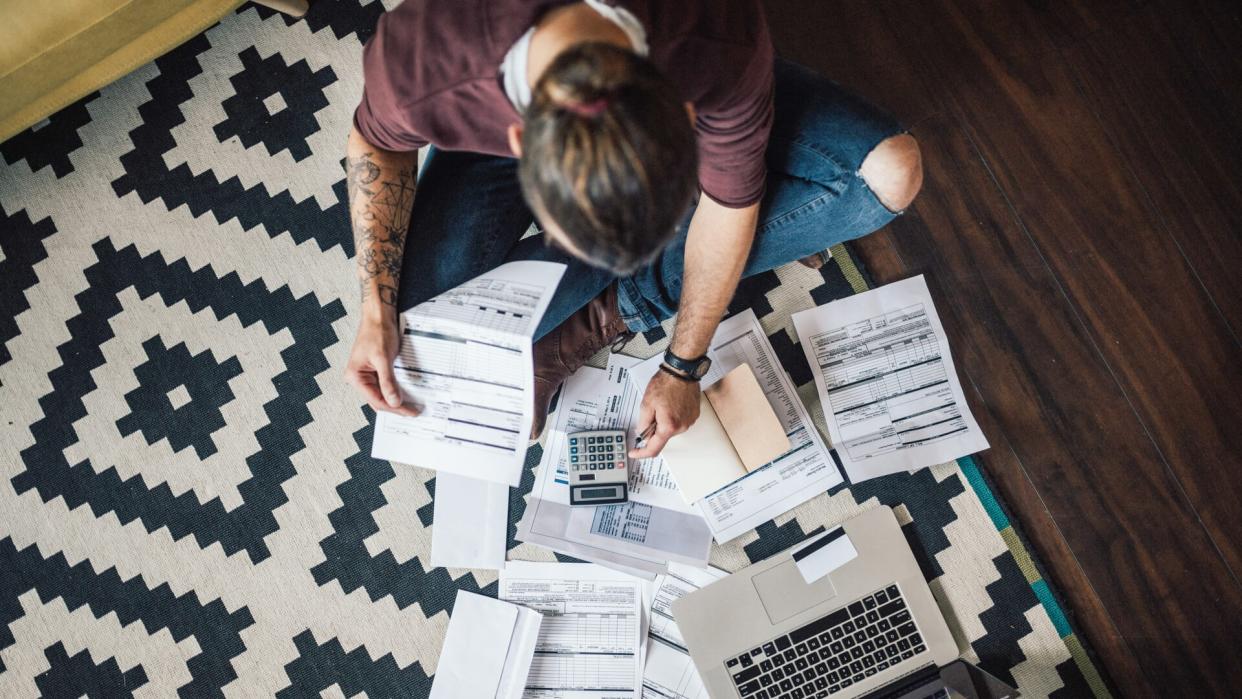

Review Your Budget

It's important to revisit your budget so you know exactly how much money you have coming in and how much you will need to cover essentials.

"A budget is key to feeling financially secure right now and determining if you can make ends meet," said Tony Drake, CFP and founder of Drake & Associates in Waukesha, Wisconsin. "Write out your budget. List all your expenses, including fixed expenses like your mortgage, car payment and cell phone bill. It should also include variable expenses, such as utility payments, groceries and entertainment. Then determine how much income you have coming in. If your expenses outweigh your income, you’re going to have to take a hard look at where you can cut, even if it’s temporary."

Read: Here’s How Much Emergency Cash You Need Stashed If an Emergency Happens

Cut Back on Nonessential Spending as Much as Possible

"During these unprecedented times there are many things you cannot control, but how you save and spend is something you can manage," said Lindsay Sacknoff, head of consumer deposit and payment products at TD Bank. "Today's financial decisions will build a cushion to help you plan for what may lie ahead."

To this end, she recommends cutting out nonessential expenses -- any expenses outside of groceries, prescriptions, rent and utilities.

"By cutting out any non-essentials from your budget, you can easily save a few hundred dollars in the coming months," Sackoff said. "Putting your gym membership on hold, canceling a streaming service you never use, and cleaning your home instead of hiring a service are all luxuries that aren’t necessary."

Reevaluate Your Spending on 'Wants'

Although it's best to cut down on nonessential spending, you might still want to allow for some "wants" in your budget -- though those "wants" might look different now than they have in the past.

"With expenses for essentials such as transportation or childcare on hold, you can look to redistribute those funds to new 'essentials' such as purchasing games or activities for your children at home, or online streaming services for TV and movies, fitness classes or a meditation app," said Shelly-Ann Eweka, a wealth management director at TIAA. "In addition to protecting your wallet, it’s important to prioritize your and your family’s mental health in this new reality."

Find Out: Biden Wants To Shut Down Credit Bureaus – What Would That Mean for You?

But Set a Budget for This Discretionary Spending

"While it's easy to assume being quarantined will automatically reduce your spending, food delivery and online shopping can cause us to rack up credit card bills quickly," said Lauren Anastasio, CFP at SoFi, a personal finance company.

She recommends setting a new budget for yourself that accounts for these discretionary expenses.

Try To Decrease Your Spending on 'Needs,' Too

See where you can save on "fixed" expenses as well.

"Look over utilities and insurance bills to make sure you're getting the best rates," said Howard Dvorkin, chairman at Debt.com. "Conserve water, electricity or gas in ways that are good for your wallet and the environment."

Reality: How the Coronavirus Outbreak Is Devastating the Livelihood of Hourly Workers

Review Your Savings

Figure out exactly how much you have in savings, between savings accounts, emergency funds, retirement accounts and other accounts.

Drake said to ask yourself, "Will you need to tap into your savings to make ends meet? If so, what are your options, and how will each option impact your financial future?”

Save as Much as Possible While You Can

"As we enter a potential period of unemployment or reduced income, we want to have the largest financial cushion possible," Anastasio said. "If you have not yet taken a reduction in pay, been furloughed or otherwise laid-off, do your best to sock away as much cash as possible with the paychecks you still have coming in."

Prioritize Your Emergency Fund

"As the COVID-19 pandemic makes clear, financial stressors can strike with minimal warning," said Greg Klingler, CFP, ChFEBC, director of wealth management for the Government Employees’ Benefit Association. "An emergency fund is a crucial part of your budget, and you may need to contribute a bit less to your savings (retirement or debt payments) and/or wants (entertainment, clothes, etc.) to establish and fund it. All Americans should maintain three to six months of expenses in liquid cash."

Money Opportunities: Capital One 360 Promotions: Best Offers, Coupons and Bonuses

Next, Prioritize Paying Down Debt

“While it might be hard to make debt payments on top of your other bills, you need to stay on top of high-interest debt, like credit card debt," Drake said. "We waste the most money on high-interest debt, so don’t let that pile up right now."

Drake recommends using the avalanche method to pay down existing debts: "Start by organizing your debt by interest rate. Prioritize your debt with the highest interest rate while still making minimum payments on the rest. Once that debt is paid, move to your next-highest interest rate."

Continue To Contribute To Retirement Savings, If Possible

Covering essentials and building up an emergency fund should be your priorities, but if you are financially able to continue contributing to your retirement savings, you should be doing so.

"Many people are facing difficult circumstances that call for scaling back, or stopping, retirement savings temporarily," Eweka said. "However, you should continue to put as much as you can into your retirement. Perhaps, that means allocating the funds you had set aside for the coming months that are now canceled, such as kids' sports activities or extracurriculars, and put that spending into savings."

Tips: Things To Cut Out Right Now To Save Money During the Health Crisis

Keep Calm and Stay Invested

With all of the market volatility, it's tempting to cash in on your portfolio before values go even lower, but Klingler advises against this.

"While you and your financial advisor should periodically assess and carefully consider rebalancing your portfolio, it’s essential to remind yourself that you’re not playing the day traders’ game: you’re investing for the long run and your long-term financial security," he said. "Patience is truly a virtue when facing the ever-present volatility of the stock market. Unfortunately, I’ve seen a great number of clients make emotional, rash decisions during market turbulence, only to see them quickly backfire, undercutting their long-term financial security and putting them on a very difficult path to recovery."

What To Do If You've Experienced Job Loss or Reduced Income

Many Americans have experienced layoffs, furloughs and reduced pay as the result of the coronavirus pandemic, so they may need to take extra steps in addition to the ones previously outlined. Here's what to do if you've experienced a decrease or loss of income.

Savings: Americans’ Savings Drop to Lowest Point in Years

Call Your Credit Card Company If You Will Be Late on a Payment

It never hurts to ask for help if you need it, Eweka said.

"Quickly prioritize which bills you can pay this month. In some cases, it's just not possible to pay all of them. If you find yourself unable to make your credit card payment, call your credit card company and see if they can give you more time and waive any interest," she said. "This can give people a little bit more time to get help."

Bad Credit: 30 Things You Do That Can Mess Up Your Credit Score

Talk To All Your Other Creditors

In addition to your credit card company, speak to your other lenders to see if they can offer assistance.

"Many lenders are prepared to offer you payment modification options or even forbearance for some of your largest expenses including your mortgage, car loan, student loans, etc.," Anastasio said.

File For Unemployment

If you've lost your job, file for unemployment ASAP.

"Filing for unemployment involves a waiting period of normally seven days, and filers can expect to see their first check/deposit processed after an additional seven days," Klingler said.

Consider Taking Out a Home Equity Line of Credit

If you don't have enough of a financial cushion to survive a job loss, and unemployment benefits won't be enough to make ends meet or won't get to you quickly enough, you will need to find additional sources of income. Klingler said that a home equity line of credit should be your first choice.

"If you have equity in your home and an open HELOC, you may be able to access this equity," he said.

Withdraw From Your 401(k) Plan

If a HELOC is not an option, you might consider borrowing from your 401(k).

“The new stimulus bill allows those under the age of 59½ to take a distribution of up to $100,000 from their 401(k) without paying a 10% penalty," Drake said. "Be sure to talk with a financial professional about your options before withdrawing money from your retirement accounts.”

Take Out a Personal Loan -- but Read the Fine Print

You might find yourself needing to take out a personal loan or line of credit during these times, but don't rush into accepting the first offer you get.

"Do your research and read the fine print," Drake said. "Fees and interest rates can add up fast, so it’s important to understand what you’re signing up for. Before taking on any form of debt, research other options."

More From GOBankingRates

Mark Evitt contributed to the reporting for this article.

This article originally appeared on GOBankingRates.com: 11 Basic Money Moves Everyone Should Make During Hard Times