Why the Supreme Court could deliver a much more fatal blow to Obamacare this time around

Any day now, the Supreme Court is set to hand down a decision in King v. Burwell, a case that centers on a key provision of the Affordable Care Act that helps provide subsidies to millions of low-income people.

It's the third major Obamacare-related case before the court in the past four terms. But if the high court rules against the Obama administration in the coming days, it could potentially deliver a much more fatal blow to President Barack Obama's signature healthcare law than it could have with previous cases.

"If the court sides with the challengers, chaos ensues, not only in insurance markets but in the political realm as well. The law could survive, but in a very weakened form," Larry Levitt, a senior vice president at the Kaiser Family Foundation, told Business Insider.

Last year, the court ruled against the administration in a case involving a relatively small provision of the law — its contraception mandate. The court ruled that family-owned corporations shouldn't have to pay for insurance that covers birth control.

In 2012, the court somewhat surprisingly sided with the administration in the end, when it held upheld the heart of the law — its mandate that individuals buy health insurance or pay a penalty.

But there's a key difference between this case and the 2012 version: Most of the law has been fully implemented for almost two years, and a decision against the government could have real effects.

A decision in favor of the challengers in the case could, depending on your viewpoint, take away health insurance from millions of people or free them from government-subsidized insurance to potentially more affordable options.

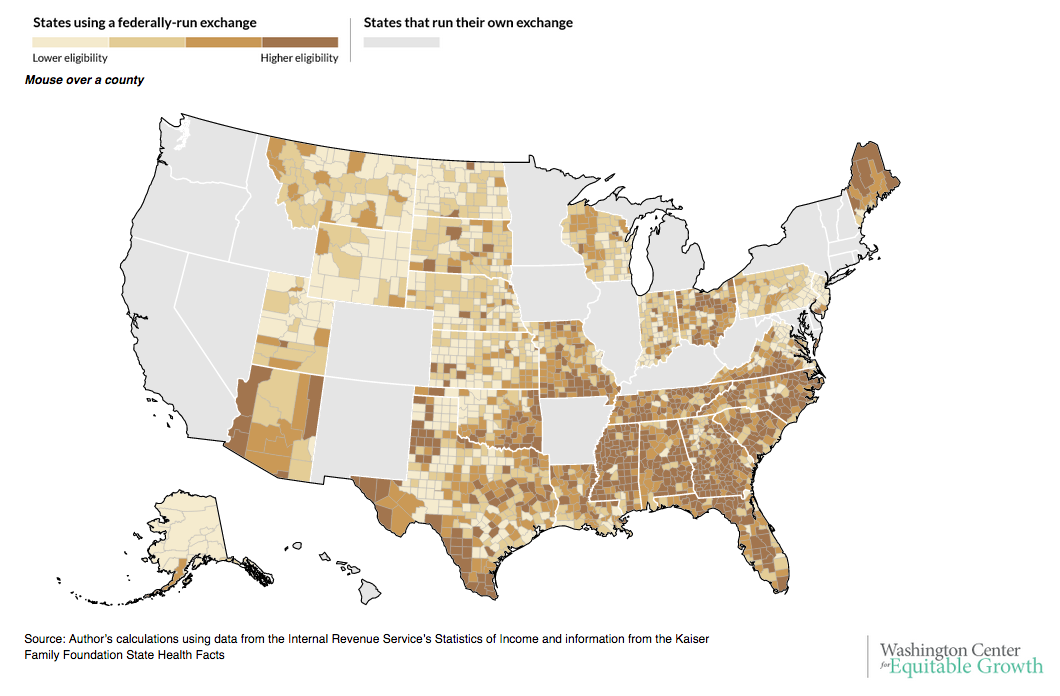

What's not debatable is that more than 6 million people could have their lives thrown into chaos because of a disruption in their health insurance. The key question in the case centers on whether the government can keep providing subsidies to help low-income people through the federal insurance marketplace.

The challengers argue the way the law was written does not allow for subsidized insurance in states where the federal government had set up insurance exchanges. Instead, the challengers argue, insurance subsidies are allowed only in states that have set up their own exchanges. They point to a clause that reads exchanges should be "established by the state," but members of Congress who were involved in writing the law have disputed this characterization. Thirty-four states currently rely on the federal marketplace.

A win for the challengers could lead to significant ramifications, and it would become a dominant theme on the 2016 campaign trail.

Michael Cannon, the Cato Institute's director of health policy and a key architect of the current challenge before the court, told Business Insider it could be an opportunity for Republicans to provide Obamacare with something of a death knell if they can propose a new law that would further unravel the president's signature healthcare law.

Cannon favors a version of legislation introduced by Rep. Paul Gosar (R-Arizona), which would exempt plans in states affected by the King v. Burwell ruling from some regulations imposed by the Affordable Care Act.

"Republicans should realize that they would not need to expand Obamacare to solve the problem," Cannon said.

Others, like Levitt, say the response to a potential win for the challengers would depend on several factors — chief among them being how those affected and the general public responds to the likely swift loss of subsidies. It would be crucial to find a way to pay for insurance before people started getting rid of their coverage.

"Like Humpty Dumpty, the individual insurance market would be hard to put back together if people lose subsidies and start dropping coverage," he said.

NOW WATCH: Here are all the best moments from Donald Trump's presidential announcement

See Also:

The uninsured rate just experienced its sharpest drop ever under Obamacare

The fate of Obamacare could reside in the hands of one of these 2 people